Carried Interest

In the Interest Of

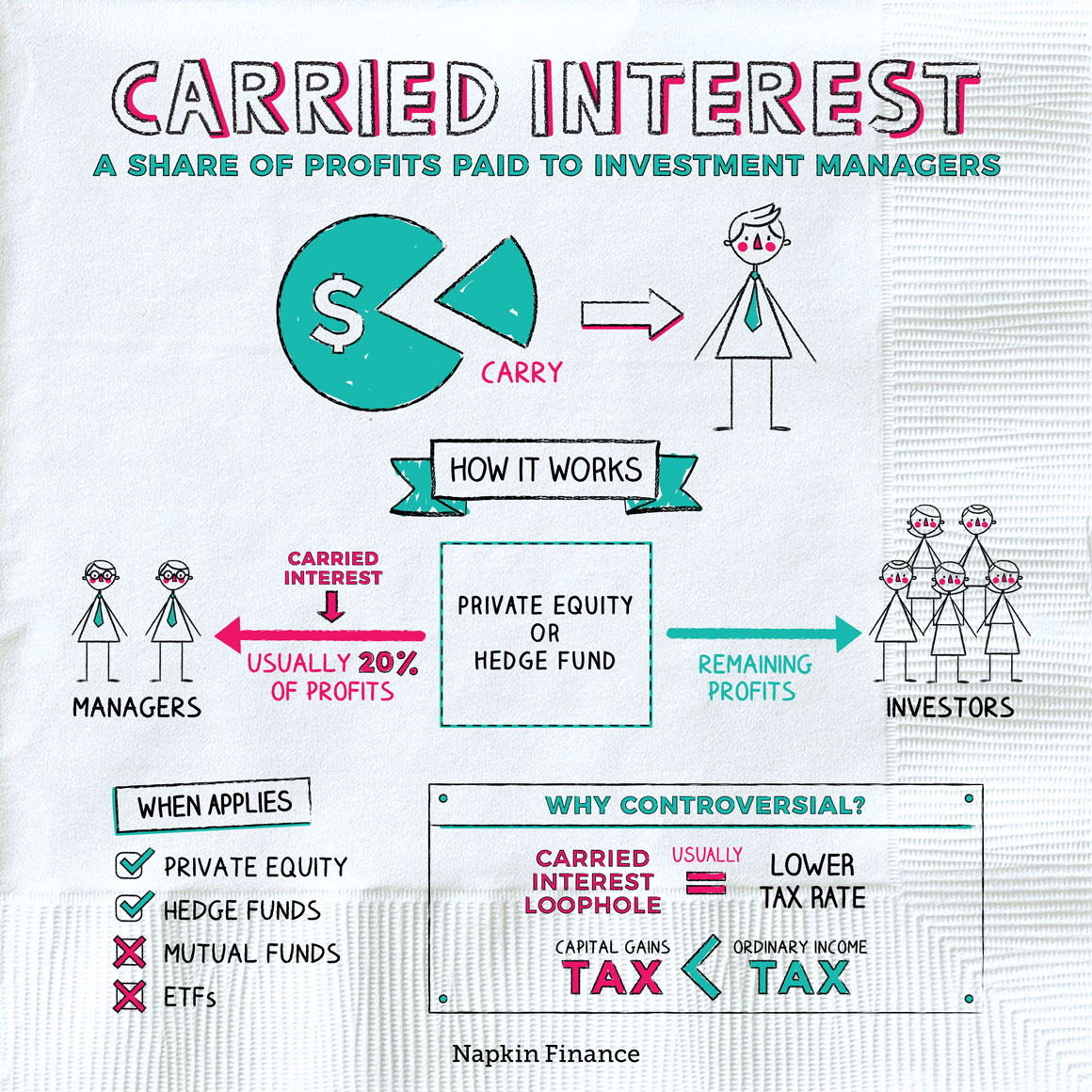

Carried interest is a share of a private equity or hedge fund’s profits that is paid to the fund’s managers. People often view this money as a performance bonus because the more the fund makes, the more profit there is for the managers to share.

Investment managers typically pay a low tax rate on the carried interest they earn—lower than what most people pay on their salaries. That’s why carried interest is controversial, and some people see it as a tax loophole.

Carried interest can apply to investment funds that are set up as partnerships. Typically, it’s relevant to private equity and hedge funds. Here’s how those work:

- Private equity funds: Make large investments in startups or struggling companies either by purchasing majority ownership or buying the companies outright. The fund managers then implement changes to make the underlying businesses more profitable.

- Hedge funds: Have flexibility to invest in a wide variety of asset classes and strategies, including commodities, options, and other derivatives, and potentially using short selling. Typically pursue aggressive, riskier strategies.

By contrast, traditional mutual funds and exchange-traded funds (ETFs) can’t pay carried interest to managers because they’re not set up as partnerships.

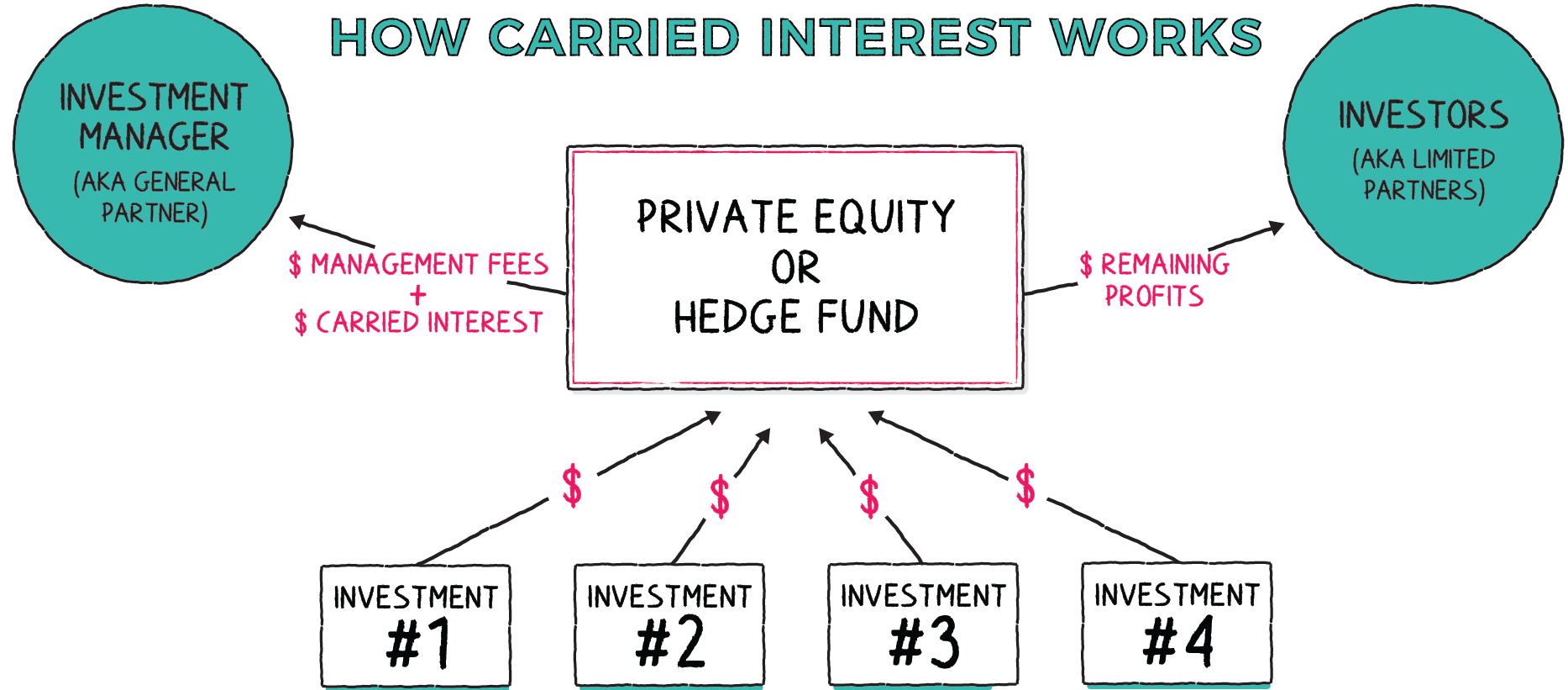

There are two types of key players in private equity and hedge funds: general partners and limited partners:

| Who | What they do | What they earn |

| General partners | Manage the fund (i.e., choose and manage investments) | Management fees plus a portion of profits (i.e., carried interest) |

| Limited partners | Invest in the fund (i.e., contribute money) | Returns left over after paying the general partners’ fees |

The amount of carried interest general partners receive can vary but is often about 20% of the fund’s profits. That’s usually paid on top of a management fee, which is often 2% of the fund’s assets.

In addition to receiving their initial investment amount back (unless the fund loses money), investors (i.e., the limited partners) receive the remaining 80% of the fund’s profits.

Here’s what the flow of dollars typically looks like in a private equity or hedge fund:

Carried interest can be a rich deal for fund managers. So many funds put some restrictions on when it can be paid in order to protect the fund’s investors’ interests. Here are some of the features funds often use:

- Hurdle rate—The fund’s managers don’t receive any carried interest unless the fund earns at least a minimum rate of return for its investors (and it may only pay carried interest on returns earned above that hurdle rate).

- High water mark—The fund pays no carried interest unless the total value of its investments exceeds its previous highest mark. This protects investors from having to “pay twice” if the fund goes up, then down, then up again.

- Clawbacks—If the fund enjoys big returns, pays out a bunch of carried interest, but then performance tanks, the managers could have to give back some of the carried interest they already received.

Managers typically continue to receive their management fees no matter how the fund is performing.

Income from carried interest is taxed at the capital gains rate, which is often much lower than the rate for ordinary income.

Some people view this as an unfair advantage for wealthy fund managers. Supporters, however, say that without the incentive of capital gains it would be difficult for startups and other companies to find investors, create jobs, and contribute to the economy.

Carried interest compensates hedge fund and private equity managers for good performance. Only funds that are structured as partnerships are able to pay carried interest. Carried interest is controversial because managers typically pay a low tax rate on these earnings.

- The Tax Cuts and Jobs Act requires funds to hold investments for three years in order for carried interest to be taxed as capital gains instead of ordinary income.

- Some funds charge higher than average carried interest rates—sometimes up to 30% of a fund’s total profits. These higher rates are called “super carry.”

- The origin of carried interest can be traced to the colleganza of medieval Venice. Under these agreements, an investor would contract with a merchant to transport certain goods, usually overseas. The merchant received a portion of profits from the sale of the goods. This is also where the “carried” comes from, since the merchant would “carry” the goods for the investor.

- General partners in a private equity or hedge fund are often paid a share of their fund’s profits. That share is called carried interest.

- Carried interest is not guaranteed. A fund typically must achieve a minimum rate of return before general partners can receive it.

- If a fund performs well but then does poorly, a general partner may have to give back some of the carried interest they already received to make up for the lower returns.

- Some people consider carried interest to be a tax loophole because fund managers often pay a low tax rate on it.