Life Insurance

Beyond the Veil

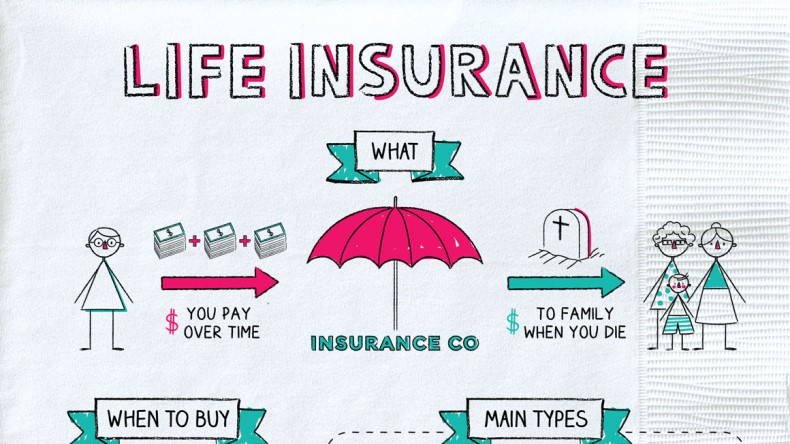

Life insurance is a contract with an insurance company. In exchange for periodic payments, the insurance company provides money to your family (or whomever you name as your beneficiary) after you die.

Life insurance helps you provide financial security for your family. Like other types of insurance, it’s meant to minimize a specific risk. In this case, you’re minimizing the risk that your family will be left in poverty if you die and can no longer provide for them.

To get this benefit, you pay a fee (known as a premium) monthly, quarterly, or annually. The insurance company sets your premium based on its estimate of how likely you are to die. Generally, the riskier you are, the higher the premium.

When weighing your risk, they’ll look at:

- Your overall health (often based on a medical exam)

- Family health history

- Occupation and hobbies

- Driving record

- Any history of smoking

Not everyone needs life insurance. If you’re young and don’t have any kids or other dependents, it might not make sense to pay for a policy. You can say the same for older people without dependents.

If you plan to have kids one day, you could buy a policy while you’re young to try and get a lower rate. The trade-off is that you’ll pay premiums over a longer period of time.

When you buy a life insurance policy, you pick the dollar value of the payout you want your beneficiaries to get when you die. This can range from thousands of dollars into the millions.

Not everyone needs a $1 million policy though. There are two main approaches to calculating how much you need:

- Income-based approach: Start with your age and figure out how many years of income you’d need to replace if you die (such as until your youngest child graduates college or until the year you’d plan to retire).

- Needs-based approach: Determine how much money your family would need to support their lifestyle if you died. Factors can include whether your partner works, the cost of educating your children, paying the mortgage, and covering outstanding debt.

One rule-of-thumb approach is to simply multiply your income by ten. But how much you actually need can vary pretty widely with your life circumstances (e.g., if you have no kids and no debt versus five kids and a hefty mortgage). With life insurance, it can make sense to go the extra mile and run the numbers.

Most life insurance falls into one of two categories:

| Permanent | Term | |

| How long does coverage last? | Forever; as long as you pay your premiums, the company will pay out your benefit no matter when you die | A set number of years; if you buy a 20-year policy but die in year 21, it won’t pay a benefit |

| How much does it cost? | More | Less |

| Can I use the money for something else? | Yes; the policy grows in value over time, and you can borrow from it | Usually no |

| What else should I know? | Some policies pay dividends that you can use to get more insurance or cut your premiums | Some policies renew automatically if you don’t die within the term; or, you can convert them to permanent policies, but that comes at a higher cost |

Life insurance can get pretty complicated. Here are some of the extra features you may run into if you’re shopping around for a policy:

- Investment options—Some types of permanent life insurance invest the cash value of your policy in savings-type options that pay low interest. Others let you invest in mutual funds that may own stocks and bonds.

- Waiver of premium—If you become disabled, you can keep your policy but don’t have to keep paying the premium.

- Accelerated death benefit—If you’re diagnosed with a terminal illness, you can receive advances against your policy.

- Guaranteed insurability—Guarantees that you can increase the value of your policy in the future (even if your health takes a turn for the worse).

Life insurance provides money to your family after you die in exchange for regular premium payments while you’re alive. The life insurance company sets your premium based on factors such as your health, age, job, and hobbies. When choosing a policy, you’ll need to decide how much coverage you want and whether you want a term or permanent life policy.

- Life insurance can bring out the worst in people, including one woman who thought she was hiring a hitman to kill her husband but accidentally hired an undercover cop instead, and a couple that tried to fake the husband’s death using a woman’s body.

- You can take out a life insurance policy on someone else. But you can’t take one out on a total stranger (because the government doesn’t want to create any incentives for you to become a professional hit).

- Life insurance provides a cash benefit to your beneficiaries when you die.

- Those without dependents or who have enough saved for expenses might not need a life insurance policy.

- There are many factors to consider when choosing a coverage amount, including your salary, debts, and the cost of educating your kids.

- Life insurance comes in two primary forms, permanent life and term life. They differ in cost, how long coverage is good for, and whether you can use funds from the policy during your lifetime.