Capital Gains Tax

The Taxman Cometh

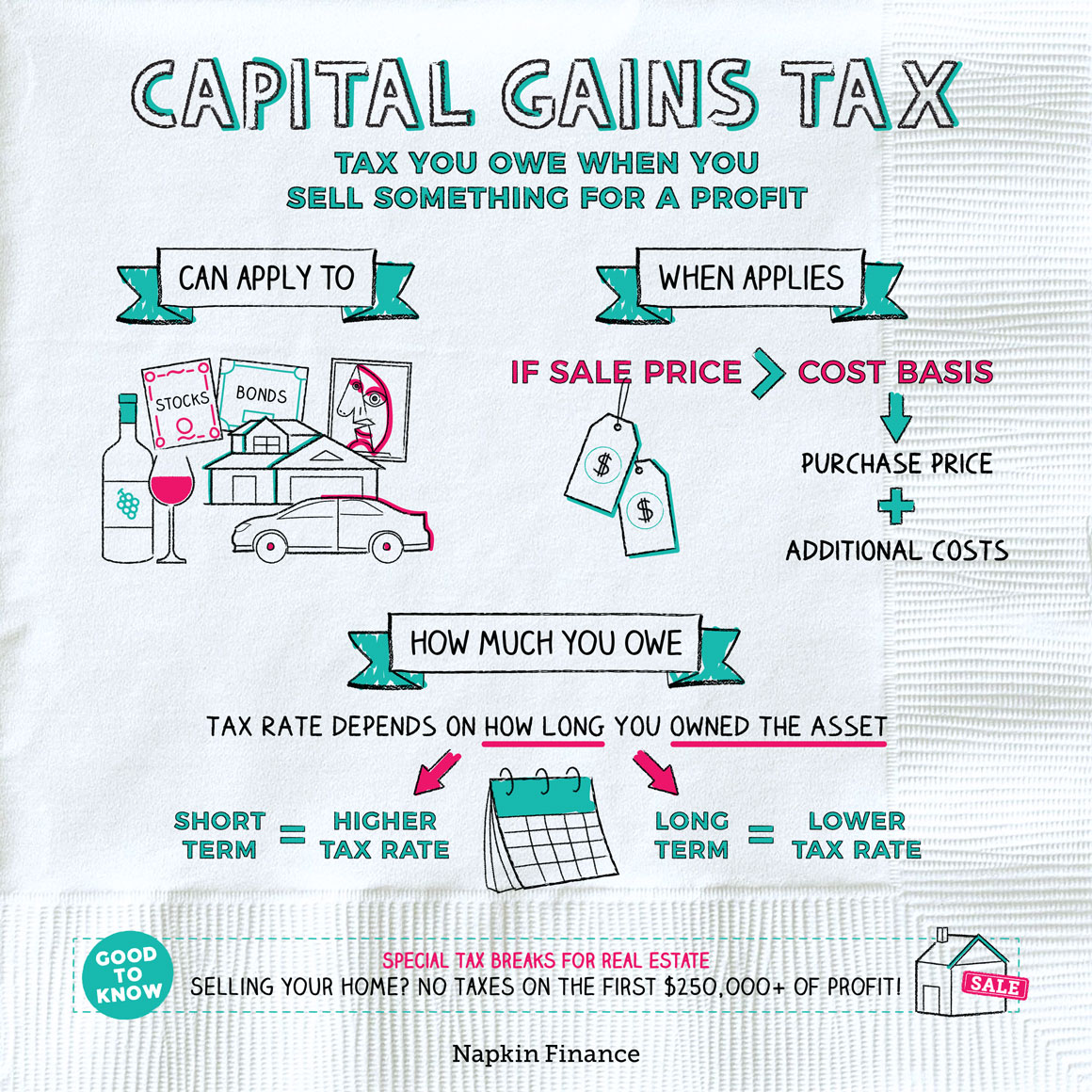

If something you own goes up in value and you sell it, then you’ve made a profit. That profit is called a capital gain, and a capital gains tax is the tax you may owe on that profit.

This tax isn’t just for wealthy investors. Anything of value sold for a profit—whether jewelry, a car, or your nerdy friend’s comic book collection—can be subject to the tax.

Capital gains tax can apply to anything of value, even if you don’t consider it an investment. More specifically, the tax often applies to:

- Stocks

- Bonds

- Real estate, whether the house you live in, your family’s vacation home, or a property you’re an investor in

- Art

- Cars

- Collectibles, such as stamps, baseball cards, or wine

- Cryptocurrencies

- Business assets, such as equipment or machinery

The tax may apply anytime you sell something for a profit.

To figure out whether you owe taxes on a sale, you first need to figure out the so-called cost basis of the item you sold. The cost basis is the amount you paid for the item—but also typically adds in taxes, shipping, and any improvements you’ve made to the item (such as adding new floors to a house or putting another gem into a ring).

If you’ve sold the item for more than your cost basis, you have a capital gain. In that case, you typically have to report the gain on your tax return, and you may owe tax on the gain.

If you’ve sold the item for less than your cost basis, you have a capital loss. Although no one likes losing money, the upside of a capital loss is that you may be able to use it to reduce your taxes—by offsetting any capital gains you have on other recent sales.

“I am proud to be paying taxes in the United States. The only thing is—I could be just as proud for half the money.“

—Arthur Godfrey

What tax rate applies depends on how long you’ve owned the asset. In general, you pay a lower tax rate for profits on items that you’ve owned for more than a year:

- Owned for one year or less—your gains are usually taxed at the same rate as your regular income (this is called the “short-term” capital gains rate).

- Owned for more than one year—your gains may be taxed at 0%, 15%, or 20% but usually at a rate lower than your regular income tax bracket (this is called the “long-term” capital gains rate).

There is an important exception to this rule. Long-term gains from the sale of so-called “collectibles”—such as stamps, jewelry, or antiques—are generally taxed at your ordinary income tax rate up to a maximum rate of 28%.

Tax rates change frequently. The exact rate that applies to a particular sale depends on the rate that was in place for that tax year. Check with the IRS website or an accountant if you’re ever in doubt!

For many people, the most expensive asset they own is a house. Whether you live in it or own investment properties, any sale could result in a capital gains tax. However, there are special rules for real estate:

- If you sell your primary residence (i.e., the home you live in), you don’t have to pay taxes on the first $250,000 of capital gain (or the first $500,000 for married couples). This only applies to the home you live in, not an investment property.

- When calculating the cost basis, you can add additional expenses, like upgrades to the property, agent commissions, or closing costs. Having a higher cost basis reduces your capital gain when you sell the property.

- If you’re selling an investment property, you can defer the taxes you owe by using what you make from the sale to buy another investment property.

You may owe a capital gains tax anytime you earn a profit from selling an asset. It’s calculated by figuring out the capital gain (the difference between the purchase price and what you sold it for) and how long you’ve held the asset. Typically, the longer you’ve owned the item, the lower the tax rate. There are special rules for real estate sales that can help you either avoid the tax or reduce what you owe.

- The highest capital gains tax rate in U.S. history was 73%. The rate was put into place by President Woodrow Wilson during World War I.

- If you buy and sell comic books just for fun, the IRS typically considers it a “hobby,” and one set of tax rules apply. If you buy and sell comic books with an aim of making a profit, the IRS may consider it a “business,” and a whole different set of rules apply.

- The capital gains tax is assessed on profit earned from selling an asset whether a house, car, collectibles, or personal property, like furniture.

- The tax rate is based on how long you’ve owned the asset and your tax bracket.

- If you have a capital loss, you might be able to use that to reduce your tax liability.

- There are special rules for real estate when it comes to capital gains that allow you to avoid the tax or reduce what you owe.