Paying Off Student Loans

Take a Load Off

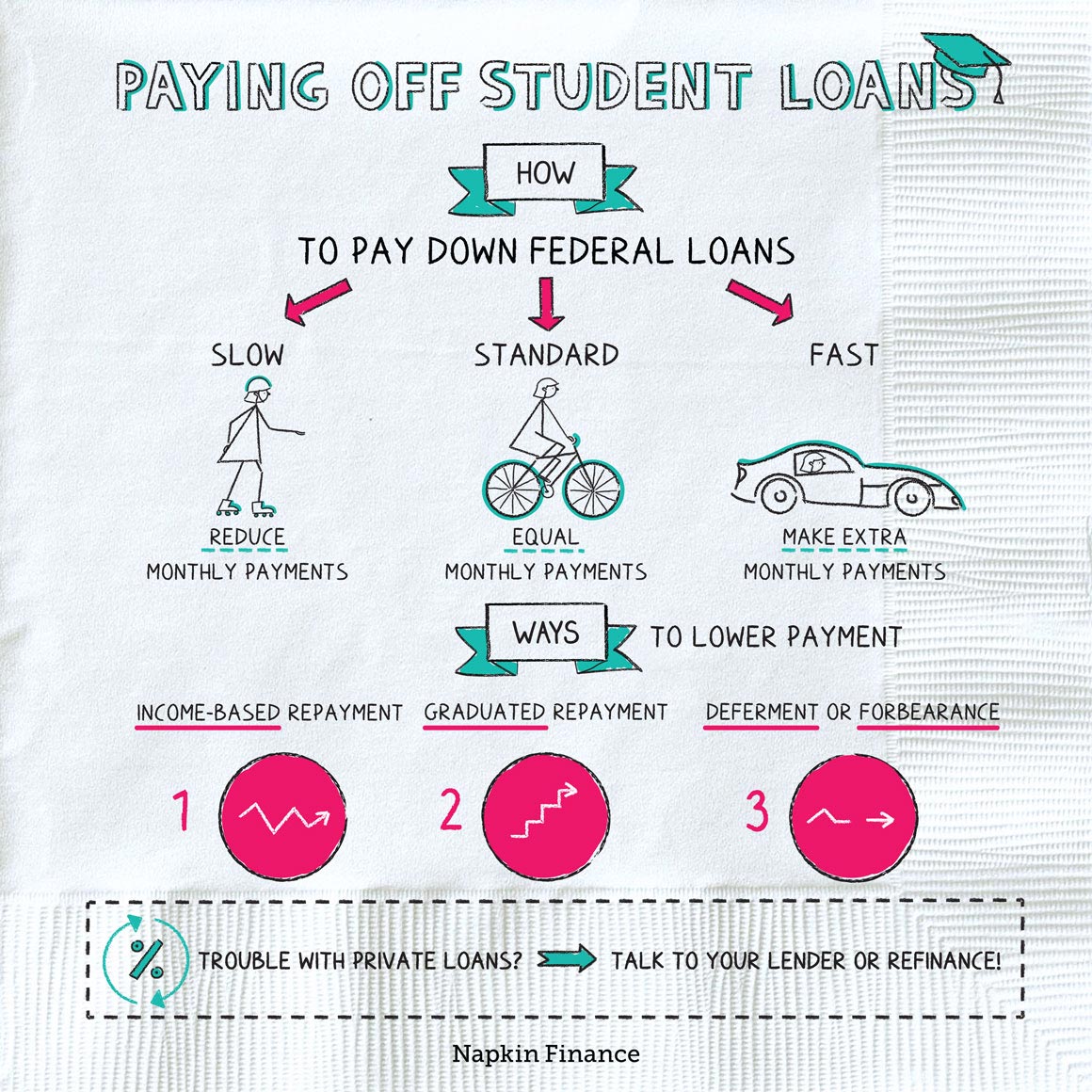

It might seem like there’s only one way to pay down your student loans (namely: slowly, painfully, and for the rest of your life.) But there are actually a few different ways you may be able to structure your payments, depending on whether you want to pay off your loans ASAP or whether you need more time.

Your federal loans will default to a ten-year repayment schedule with equal payments. That’s great if you’re making grown-up money as soon as you graduate, but some find it hard to make payments in the first few years.

With private loans, you probably agreed to a loan term and payment schedule when you took out the loan. These terms can vary widely based on the lender and the details of your situation (such as how much you’re borrowing and whether a parent is cosigning).

If you can afford to, consider making more than the minimum monthly payment on your loans (whether federal or private) because you’ll save money on interest by doing so.

If you have multiple loans, consider paying anything extra toward the loan with the highest interest rate first (probably any private loans you have).

If you’re having trouble making your payments, your options depend on what types of loans you have. For federal loans, they include:

- Income-based or income-contingent repayment—Payments will be based on your income. If your salary goes up, you’ll pay down your loans faster, but if not, you won’t drown in your bills.

- Graduated repayment or extended graduated repayment—With these plans, your payments start low and then slowly increase according to a preset schedule.

- Deferment or forbearance—Either can give you a temporary break from payments, but you must apply and meet eligibility requirements. (And neither dings your credit score—so they’re much better options than simply skipping a payment.)

If you work in public service, you could even qualify for outright forgiveness of your federal loans after a certain number of years.

If you’re struggling with your private loans, you may be able to talk to your lender to get a temporary break or to adjust your payment terms. If not, your main option will be to try to refinance your loans to:

- A lower interest rate, which could save you money in total and lower your monthly bill.

- A longer payment term, which will increase your total but can lower what you pay each month.

To quicken your progress while you’re on the road to that glorious, yet elusive payoff date, be sure to:

- Make extra payments anytime you can: If you get extra unexpected money, put it toward your loan even if you’re still in school or in your grace period.

- Put your payments on autopilot: If you can, set up automatic payments from your checking or savings account. Some loan servicers even reduce your interest rate if you do.

- Consider all your options: The standard plan might be the right option for you, but it might not, so evaluate all your repayment options.

At the same time, make sure you don’t:

- Skip payments: Your student loans show up on your credit report, so missed payments might damage your credit score and make it harder to borrow in the future.

- Pay for help: Go directly to your loan servicer for free assistance if you need help rather than a debt-settlement company or other third party that may promise to “fix” your debt problems in exchange for a fee.

Federal and private loans come with standard repayment plans. But if your current payment setup isn’t working for you, there’s a good chance you can negotiate a change—such as with income-based repayment, refinancing, or even taking a temporary deferment. No matter what you choose, it’s important to work with your lender if you’re having trouble instead of skipping payments.

- Want to pay off your loans fast? Try becoming a software developer, which typically ranks as a top-paying career option for new grads.

- A common myth is that student loans can never be discharged in bankruptcy. In fact, about 40% of bankruptcy filers who ask to have their loans discharged succeed (though you have to meet strict eligibility requirements).

- Barack and Michelle Obama didn’t finish paying off their student loans until they were in their 40s.

- Your student loans will generally default to a certain payment structure—such as ten years of equal payments for federal loans.

- However, there are often ways of restructuring your payments depending on whether you’re looking to reduce your monthly bills or pay off your loans as soon as you can.

- If you can afford to, paying extra toward your loans can save you money in interest and help you become debt free even faster.

- If you’re struggling under your federal student loans, switching to an income-based or graduated repayment plan may give you some breathing room.

- Private loans typically don’t offer as many payment choices, but refinancing could reduce your interest rate or lower your monthly payments.