Buy vs. Lease a Car

Joy Ride

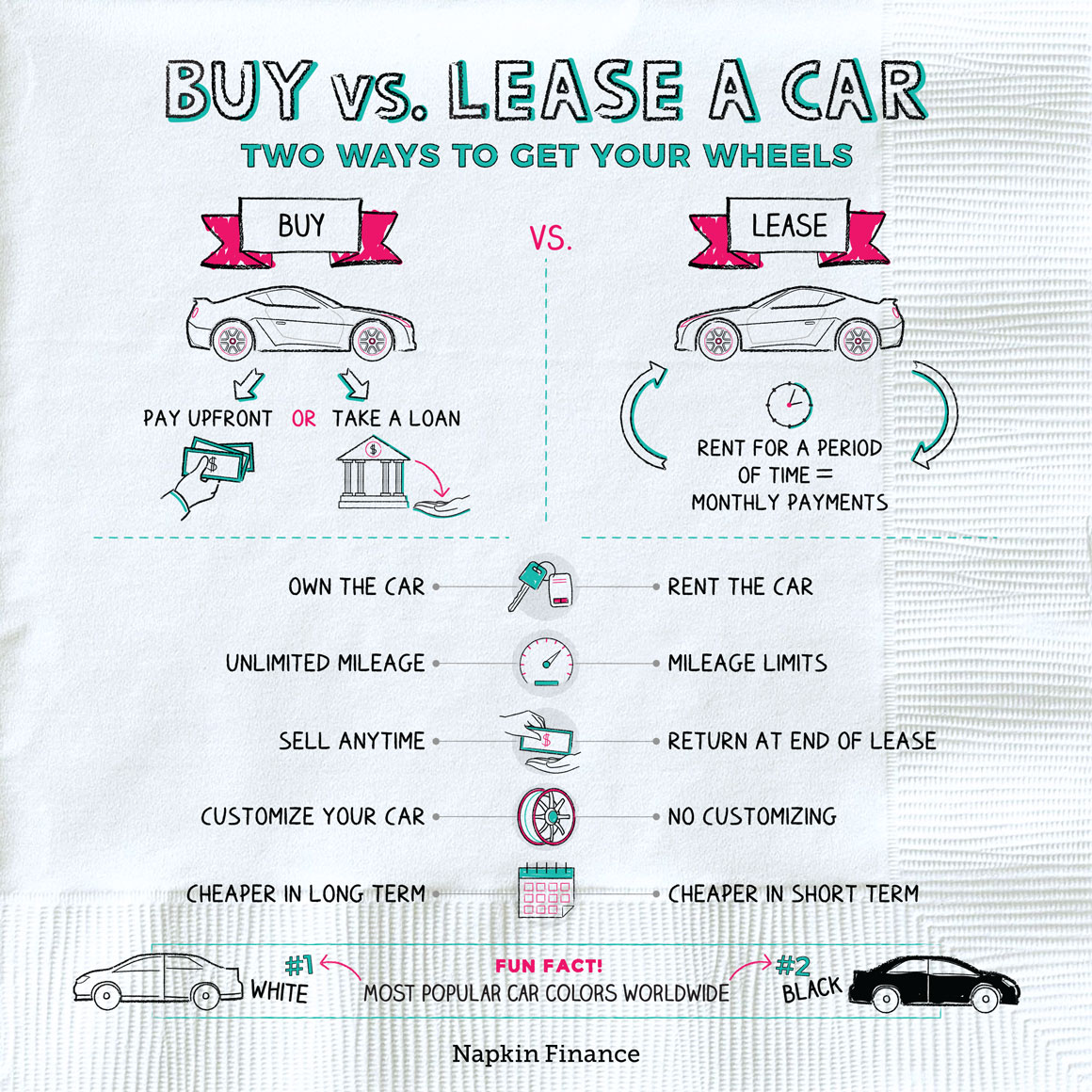

When you need a car, you have two options: buy or lease.

If you buy a car, you own it either by paying the full price up front or financing it with a loan. If you lease, you are renting the car for a set amount of time, and you have to either return it or buy it at the end of the lease term.

Buying is usually the more expensive option initially, but you own the car and can do whatever you want with it. Custom stereo? You got it. New paint job? Definitely. Monthly cross-country road trip? If that’s your thing, sure, why not.

Here’s what else you need to weigh:

| Pros of buying | Cons of buying |

| You own the car | Higher monthly payments initially |

| Unlimited mileage | Bigger down payment |

| Sell the car whenever you want | Loses value over time |

| Customize the vehicle any way you like | Maintenance costs |

“Everything in life is somewhere else, and you get there in a car.“

—E. B. White

Leasing can be more affordable on a monthly basis than buying, at least initially, but because you don’t own it there are restrictions on how you can use the car.

When you lease a car, you don’t pay the full price of the vehicle. Instead, you typically make a small down payment (there may also be some up-front fees) and then pay a set amount every month for the term of the lease. Your monthly payment reflects the lease’s interest rate plus the car’s depreciation that happens during your lease term (i.e., how much of its value it loses over that time).

There are other pros and cons to leasing, including:

| Pros of leasing | Cons of leasing |

| Lower monthly payments initially | No equity in the car (and you can’t sell it) |

| Easy trade-in (new cars on the regular!) | You always have a car payment |

| Usually covered by a warranty | The dealer might charge you for excessive wear and tear |

| Low (or sometimes no) down payment | Limited number of miles and fees for anything extra |

If you’re not sure what to choose, one option is to lease now and buy at the end of the lease term. This might be a good option if you:

- Have less to put toward a monthly payment now than you might in the future

- Really like the car

- Are likely to put a lot of miles on the car or leave it in bad shape (in which case you would owe penalties to the dealer if you turn it in at the end of your lease term)

On the other hand, if you don’t like the car, want something different, and have kept the car in great shape, you can turn it in and get a different vehicle.

Here are some issues to take into consideration when you’re making the buy-versus-lease decision:

- Cost

-

- Leasing is typically more affordable in the short term due to its lower monthly payments.

- Buying is often a better value over the long term, particularly if you’ll plan to hold on to the car as it ages.

- Customization

-

- You can’t make any modifications to a leased vehicle.

- Buying might be for you if you’re particular about the exact make and model of the car you drive along with its features.

- How much you’ll drive it

-

- You’ll face mileage limits if you lease.

- If you buy, how much you drive the car will be entirely up to you. If you drive a lot, buying is likely the better choice.

- How long you’re planning to use the car

-

- If you just need a car for a little while, go for the lease and walk away when your lease ends.

- If you’re in it for the long haul, take the plunge and buy.

- Responsibility

-

- If you feel confident you’ll be able to keep the car in good shape, leasing could be right for you.

- If you’re not good at taking care of a car, consider buying. You could face penalties on excessive wear and tear on a lease.

When you need a car, you can buy or lease. Buying requires either an up-front payment for the total cost or financing the purchase with an auto loan. Leasing is more like a rental, and your monthly payment is based on depreciation during the lease term plus taxes, fees, and interest.

- In Churchill, Manitoba, residents leave their car doors unlocked in case someone needs to make a quick escape from a polar bear.

- White is by far the most popular car color in the world, with black coming in second and gray third.

- Buying and leasing are two options available when you need a car.

- When you buy a car, you own it. When you lease a car, you’re renting it from the dealer until the end of your lease term.

- Whether to buy or lease may depend on how much money you have available up front, how long you plan to use the car, and personal preference.