Getting Out of Credit Card Debt

Pay the Piper

Credit card debt can be overwhelming. As interest accrues, your balances may keep increasing even if you’re making regular payments. You may even start to feel like your debts are beyond your control.

But getting out of credit card debt—even significant debt—is possible. The secret is to make a workable plan that you can stick to until your last account is fully paid off.

The first step in getting out of credit card debt is figuring out how much you owe and how many cards you need to pay off. Here’s how:

- Step one: Make a list of all your credit cards.

- You can’t get a handle on your debts until you know exactly which accounts need to be addressed.

- Step two: Figure out your balances and interest rates.

- Laying out your balances and how much interest you’re being charged on each can help you decide on the best approach.

- Step three: Pay off any low-hanging fruit.

- When you review your accounts, you may realize that one or two have fairly low balances. If you’re able to pay these off in full, it’s a good idea to clear them as quickly as possible, especially if they charge high interest.

- Step four: Make a plan for the rest.

- Coming up with a plan of action can reduce the stress you’re feeling and make you feel more in control.

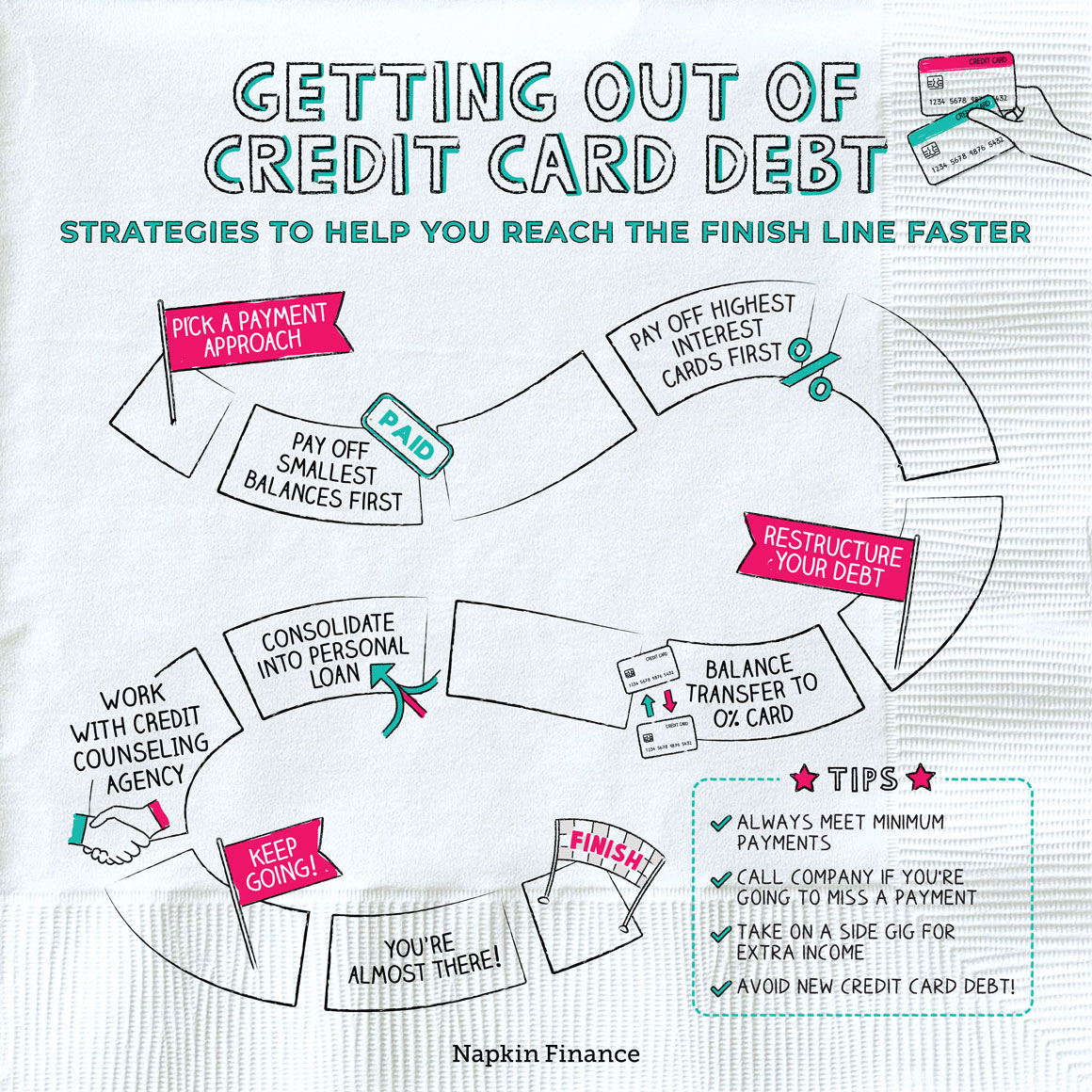

As you’re chipping away at your balances, you may need to decide which cards to prioritize. Although you should always make at least the minimum payment on all your cards (to protect your credit score), choosing just one or two accounts to tackle aggressively can help you stay focused.

There are two main approaches to prioritizing your debt payments:

| Snowball method | Avalanche method | |

| How it works | Target your smallest balance first. After that card is paid off, move on to the next smallest balance, and so on. | Prioritize your highest interest balance, such as your credit card with the highest rate. Once that’s paid off in full, focus on the next-highest interest card, etc. |

| Why it works | By helping you quickly start paying off accounts in full, it can help you build momentum and confidence. | By targeting your most expensive debts first, it helps you save money and quickly reduce any debts that could be spiraling out of control. |

Of course, those payment approaches don’t magically reduce how much you owe. If you need heavier duty help, consider a strategy that can help you restructure your credit card debt:

| Balance transfer | Consolidate | Credit counseling | |

| How it works | Transfer existing balances onto a card with an introductory 0% rate. | Use a new personal loan to pay off your credit card balances. | Work with a nonprofit agency that can help you come up with a plan. |

| Pros |

|

|

|

| Cons |

|

|

|

| May be best if | You’re sure you can pay everything off before the 0% rate is up. | You can obtain a new loan with a reasonable interest rate. | You feel too overwhelmed to go it alone. |

Any of those strategies can come with serious potential risks (including risks to your credit score). Think carefully and make sure you’re certain that a given path is right for you before you apply for a new line of credit or commit to working with a counseling agency.

Here are some other points to keep in mind while you’re whittling down your credit card balances:

- Keep making at least your minimum monthly payments on all debts and bills no matter what

- If you can’t pay, contact your credit card companies directly to ask whether they can temporarily suspend payments or modify your repayment plan

- Consider ways to boost your income so that you can put even more money toward your card balances—like selling your old stuff or taking on a side gig

- Avoid taking on new debt while you’re in repayment mode, and keep tight reins on your overall spending

And remember that there is a light at the end of the tunnel of all your hard work. It may not be the most fun-filled experience of your life, but killing your credit card debt is a major accomplishment to be proud of.

Carrying balances on high-rate credit cards can quickly become overwhelming. Getting out of credit card debt can entail getting a good handle on what you actually owe, coming up with a payment strategy, or even considering more drastic approaches, like obtaining a personal loan or working with a credit counselor.

- A quarter of Americans say their credit card balances are a daily source of stress.

- There are almost 500 million credit cards in circulation in the U.S., or more than one for every person.

- Getting out of credit card debt is a challenge, but getting organized and choosing the right payment strategy can help.

- One approach is to tackle your smallest debts first so that you can quickly close some accounts, while another is to first prioritize your highest interest rate card.

- If you need more help, you can also consider doing a balance transfer, refinancing your credit card debt into a personal loan, or working with a credit counseling agency. However, each of these approaches comes with risks.

- No matter what, make sure that you continue to always meet at least the minimum payment on all your cards and other bills.