Estate Tax

Death and Taxes

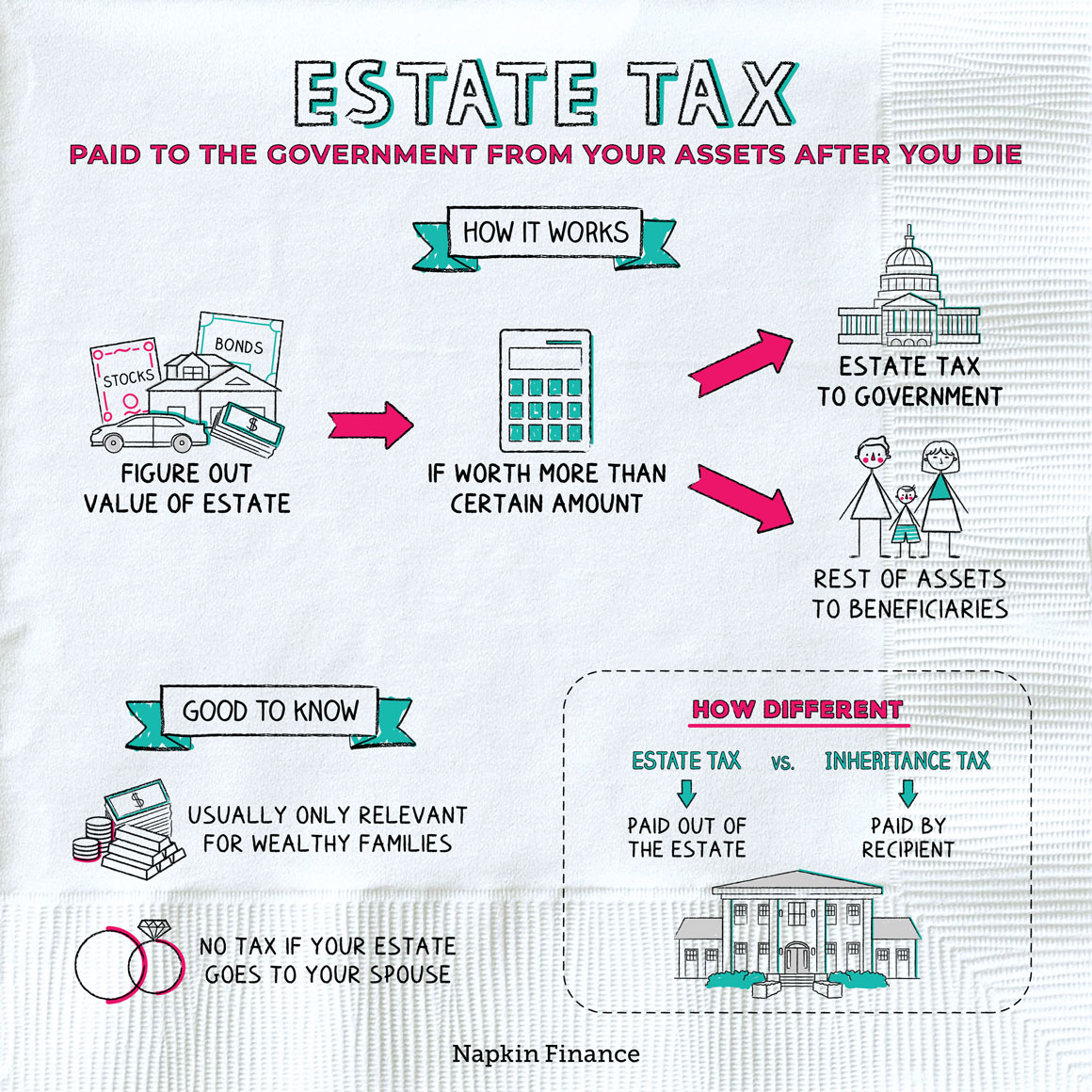

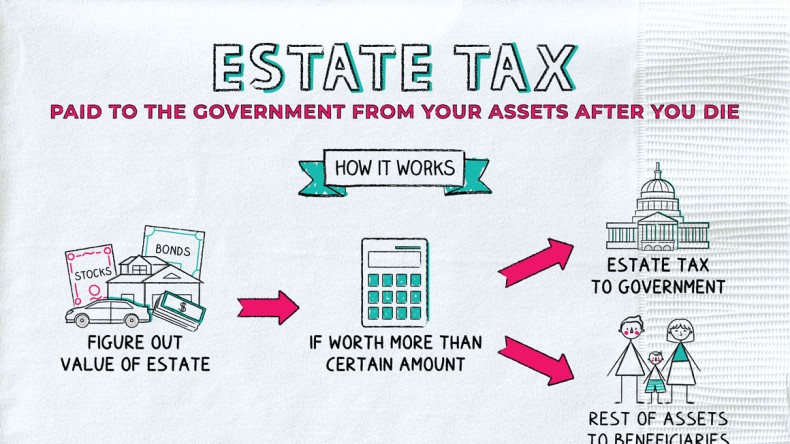

An estate tax is an amount that may be paid from your assets to the government after you die.

It’s typically only a concern for people who have at least $1 million in assets or more.

An estate tax is sometimes called a “death tax.” It’s what your estate (which is the total sum of your assets—think cash, stocks, real estate, etc.) must pay after you die before your friends and loved ones can collect whatever you left them.

The federal government and around a dozen states have an estate tax.

The estate tax technically applies to everyone, but it’s rarely actually paid in practice.

That’s mainly because it only applies to estates that are larger than a certain cutoff level. If your estate is worth less than the cutoff, your estate owes nothing.

In 2021, the federal exemption was $11.7 million (individual states set their own thresholds, which are often lower). That means only estates valued at more than that amount had to pay any taxes, and they only owed taxes on anything above that number.

One other important caveat: You won’t face a tax if your estate goes entirely to your spouse.

The federal government and individual states have different estate tax rates.

- Federal: The maximum rate is 40% of the estate’s value. But because of deductions and credits (and our generally complicated tax code), the average effective rate is closer to 17%.

- State: Rates vary state by state, but they top out at 20%

Anything you own or hold an interest in before you die may be counted as part of your taxable estate. This includes cash, stocks, real estate, some types of trusts, and businesses.

When someone dies, their “executor” is in charge of settling their financial affairs (people often name an executor in their will, or a court may appoint someone). It’s the executor’s job to add up the value of the estate and then subtract for deductions and credits. These may be available for:

- Mortgages and other debts

- Fees to manage your estate

- Donations to charity

After that, if your estate is still worth more than the exemption, it will owe taxes.

Wealthy families often try to reduce the amount of estate taxes they’ll owe. There are a few typical tools and strategies they may use to do so, including:

- Giving money to their kids or grandkids while they’re still alive

- Putting assets into an irrevocable trust

- Donating to charity

People sometimes confuse estate taxes with inheritance taxes. They’re both charged because someone died, but there are some key differences.

| Estate tax | Inheritance tax | |

| Who owes it | The estate of the person who died | The person receiving the inheritance |

| What assets it applies to | The total value of the estate | The value of the inheritance |

| Who charges it |

|

|

An estate tax is money paid from your estate to the federal or state government after you die. Your estate has to pay this before your assets can be transferred to your beneficiaries. However, most estates don’t have to pay any tax because it only applies to estates that are worth more than a certain minimum value.

- The worst states to live in when you die are Massachusetts and Oregon. They charge a tax on estates worth $1 million or more.

- Before 2001, all 50 states and the District of Columbia had some form of their own estate tax.

- Only around two out of every 1,000 estates end up paying estate taxes. Those that do pay shell out around one-sixth of the estate’s value.

- The estate tax is an amount that your estate must pay before your family and friends can receive whatever you’ve left to them.

- The federal government and about a dozen states have an estate tax.

- Most estates don’t pay the tax because it’s only charged on estates that are larger than some minimum level.

- The tax also generally doesn’t apply if your whole estate goes to your spouse.

- Estate taxes are paid out of the assets of the person who died. Inheritance taxes, by contrast, must be paid by the person who inherits the assets.