Lesson 3: Savings versus Investments

Once you start accumulating assets, you’ll have to decide what to do with your money. The right choice usually depends on what your goal is for your money and how far away that goal is. Savings are for short-term cash needs, while investments are generally for longer-term goals.

Savings

Savings are for two things: your emergency fund and any near-term goals.

An emergency fund is your just-in-case money—funds that will cover your expenses if you were to lose your job or face an unforeseen financial demand, such as a large medical bill. You should generally keep six months of living expenses stashed in your emergency fund. If you’ve been saving for a long-term goal, such as a home purchase or a wedding, and you’re within one to two years of that goal, then you should keep this money stashed in savings too.

| Savings accounts |

|

| Money market accounts |

|

| Certificates of deposit |

|

| T-Bills |

|

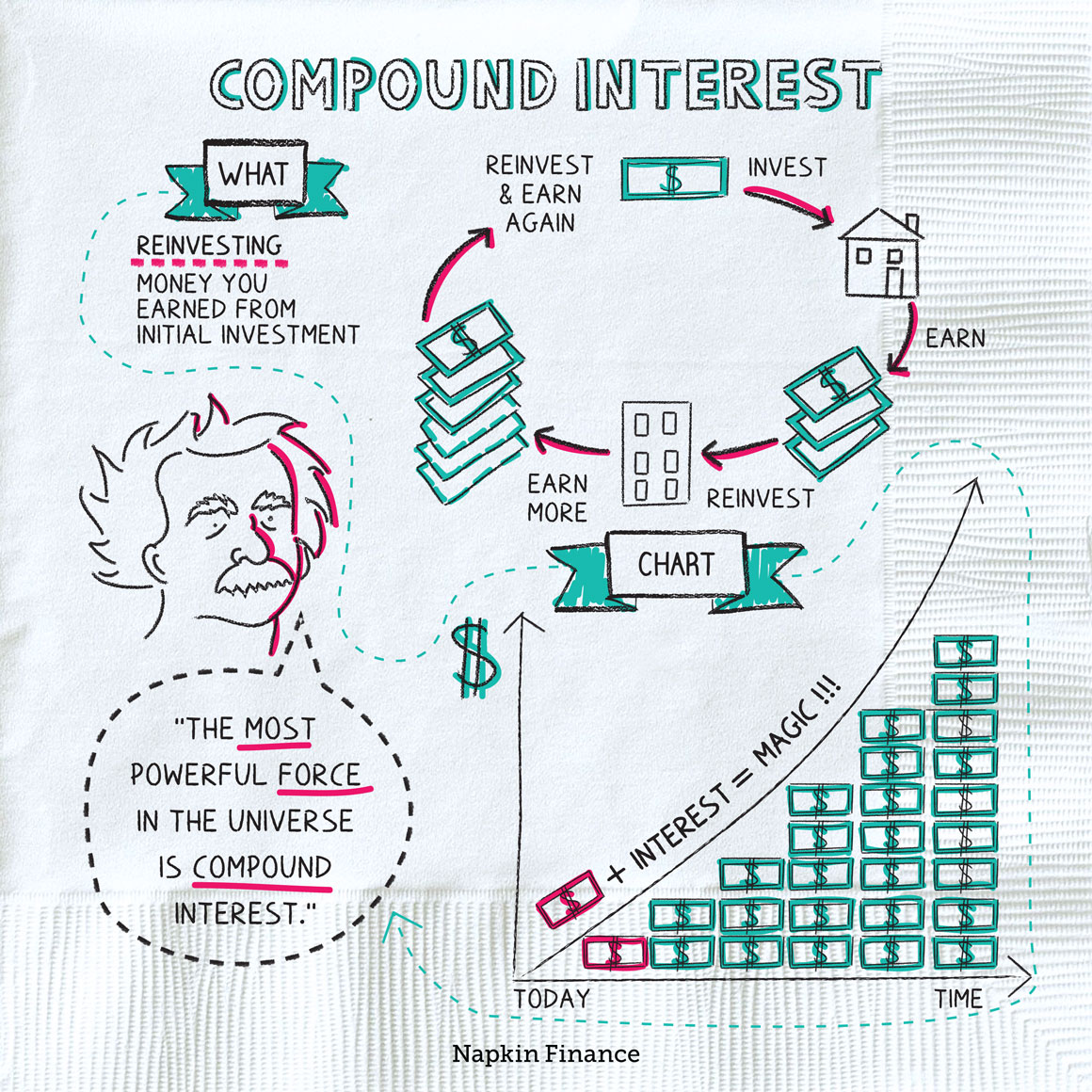

Compound Interest

How is it possible to turn your money into more money? With the magic of compound interest.

Investments

Investing can be risky, but that’s no reason to avoid it. You’ll earn a better return, meaning more compounding and faster-growing account values, with investments than you will with savings. But investments can gain or lose money in the short term. That’s why investing is generally only for money that you don’t expect to need within the next one to two years.

Long-term goals you should invest for:

- Retirement

- Your children’s college

- Home down payment, wedding, or car purchase, if these goals are at least two or more years away