Lesson 7: Leaving a Legacy

Planning for retirement can also give you a chance to start thinking about what you might (eventually) want your last wishes to be. Experts recommend that you put some end-of-life plans in place even if you’re young and healthy—because the unexpected can happen to anyone.

Benefits

Although you might think that estate planning is only relevant for the ultrarich, it can have advantages for those of more modest means too. The benefits can include:

- Making sure your kids, pets, or other dependents will be taken care of

- Having a say in who gets your stuff

- Reducing the chance of conflict among your loved ones

- Avoiding court battles

- Helping money and other assets move to your chosen heirs faster

- Potentially even reducing taxes on your estate

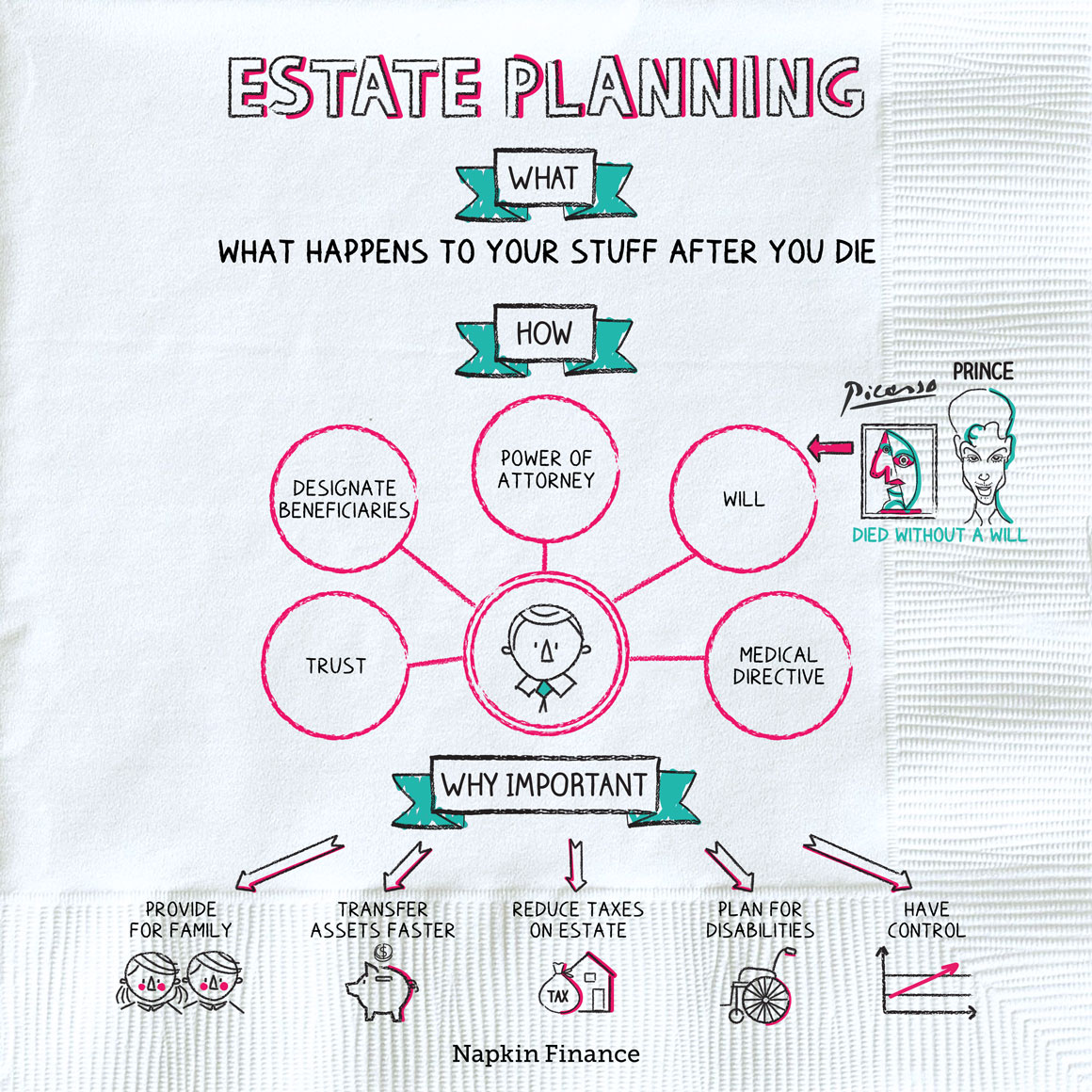

What it includes

Your estate plan will likely consist of a number of legal documents. Some of these you can take care of on your own, while others may require the help of a professional, such as a lawyer:

| What | What it is | Good to know |

| Will | A document that lays out your wishes and plans for your assets and dependents. | A will has to meet certain standards for it to be legally enforceable, so consider getting an expert’s help in crafting one. |

| Beneficiary designations | The names you put on your retirement account forms—which say who should inherit your account if you die. | You should always make sure to fill these in (and update them regularly) because if these designations say one thing and your will says another, the designations will win out. |

| Power of attorney or

advance directive |

A document stating who can make decisions on your behalf if you’re unable to make them yourself (i.e., for medical reasons). | If doctors can’t find a family member to make decisions for you in a crisis, a court may appoint someone. That’s why this is good to have even if you’re young and healthy. |

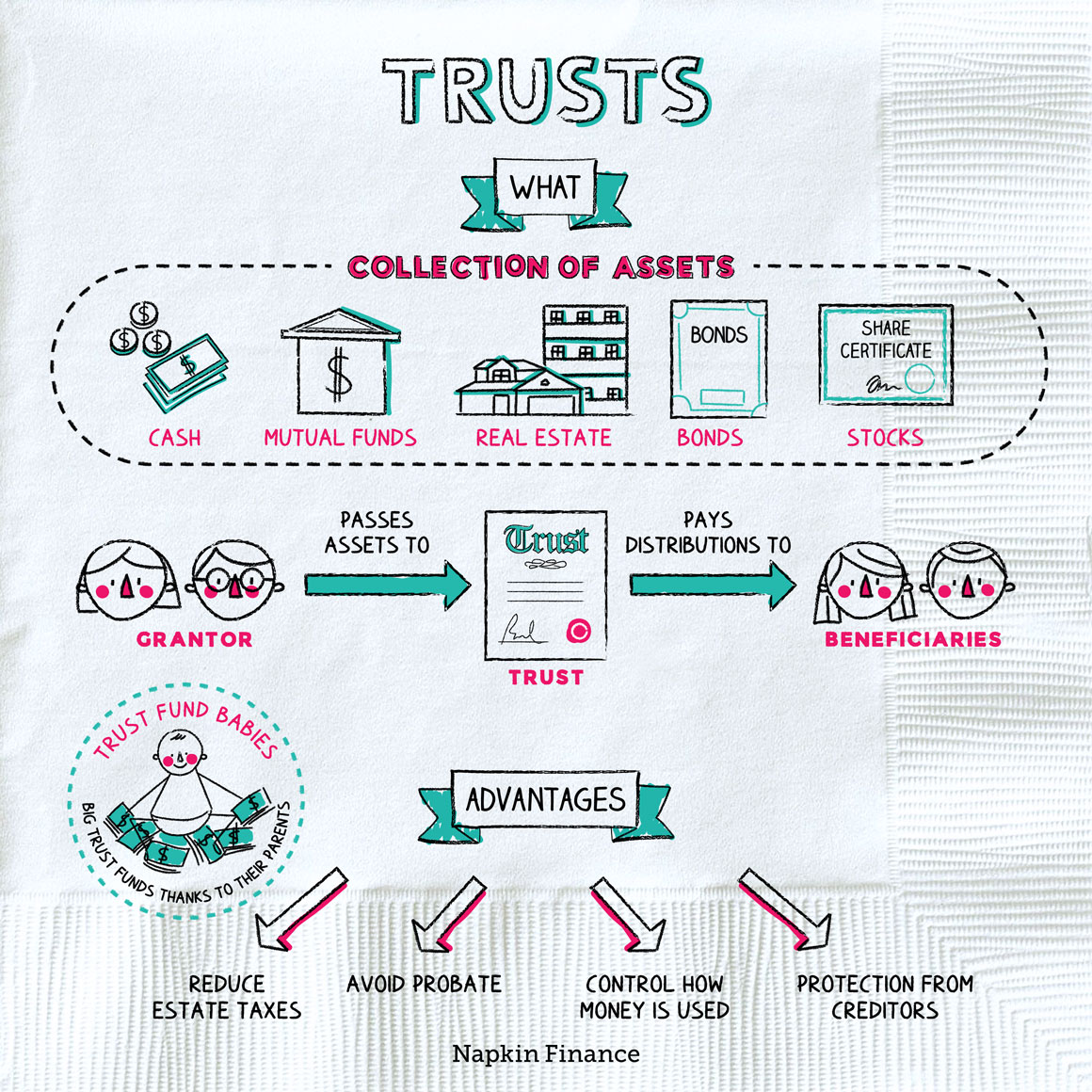

| Trust | A legal arrangement that can be used to move some assets out of your estate. | Typically only used by (or necessary for) the wealthy. |

Giving back

Estate planning can also help you plan ways to leave a lasting impact on the world. For families with high levels of wealth, there are more complex strategies available that can help reduce taxes while also leaving a large gift—such as by using certain types of trusts.

But anyone can consider setting aside some of their assets to go to a good cause when they die. If you want to leave a legacy and your means are more modest, you can consider:

- Leaving cash to a charitable organization

- Donating appreciated stock to a charity—which comes with extra tax perks but isn’t complex to set up

- Naming a charity as the beneficiary of one of your retirement accounts

Good to know

Once you have your estate plan in place, be sure to check in on it once a year—or anytime you go through a major life change, such as marriage or divorce or experience a birth or death in your family—to make sure it still reflects your current wishes.