Tax Loss Harvesting

Cut Your Losses

Tax loss harvesting is a trading strategy investors can use to try to reduce their taxes.

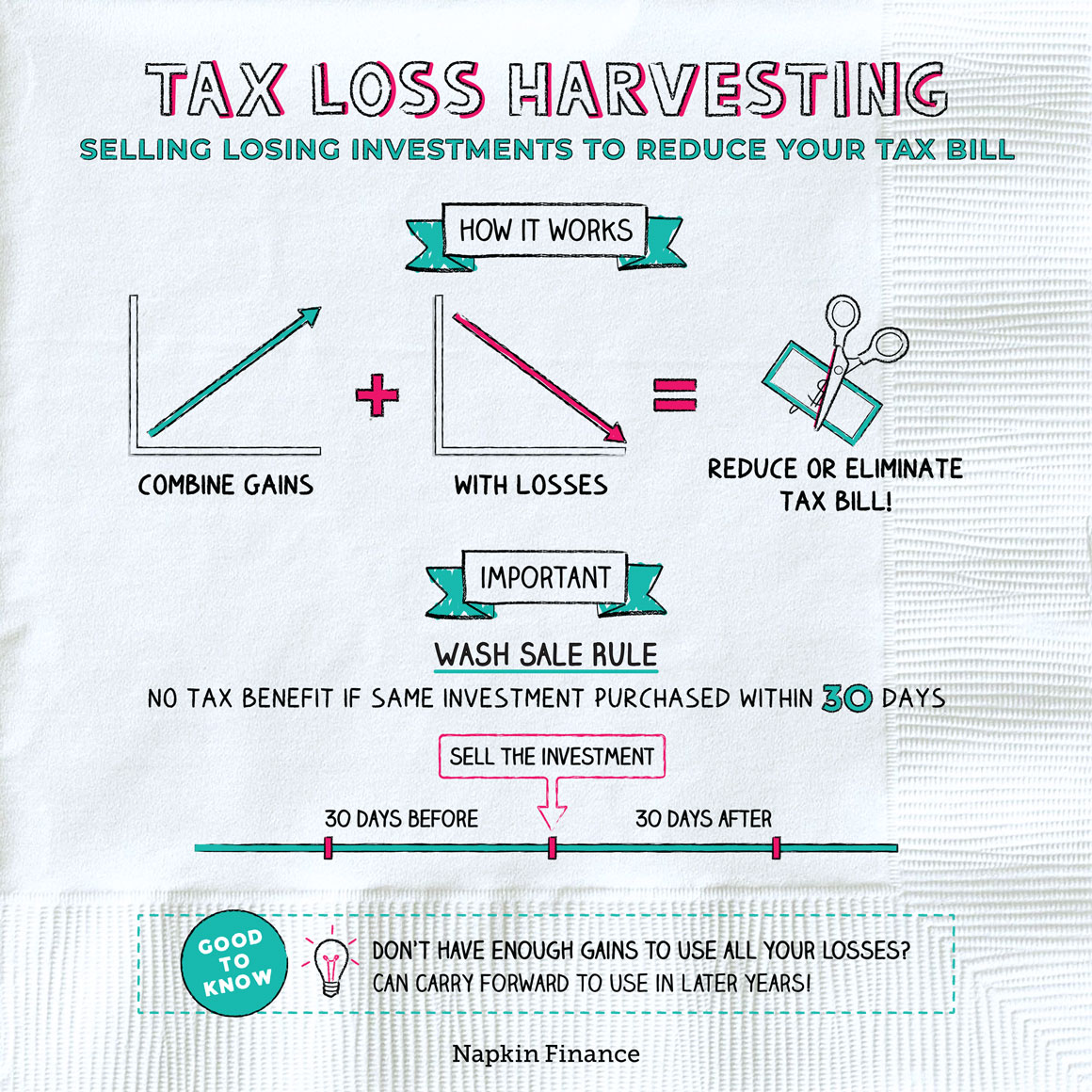

It’s a way of using your losses on some investments to offset your profits on others. The end result can be a lower tax bill.

In general, if you sell an investment for a profit you owe taxes on your gains. However, the IRS lets you use losses on investments to offset the gains you’ve earned on others.

So, if your portfolio also contains an investment that’s fallen in price since you bought it, you can sell that investment and use the loss to offset your taxable capital gains.

Tax loss harvesting is when investors strategically sell investments that have fallen in price so that they can use those losses to reduce their taxes.

Tax loss harvesting only works with realized losses, not unrealized ones. Here’s the difference:

- Realized: You sell a stock for a lower price than what you paid for it. By selling it, you realize the loss.

- Unrealized: A stock you own has fallen in price but you haven’t sold it. Because it could still recover, it’s an unrealized loss.

So if your portfolio is down in the dumps at the end of the year but you haven’t sold anything, then you don’t have any losses you can use on your taxes.

While it’s nice to get a little something for a crummy investment, it’s not always the right strategy.

| Pros | Cons |

| Reduce your capital gains taxes | Pay transaction fees to sell |

| Possibly improve your big-picture returns, after accounting for taxes | Might miss out on future gains |

| Cut your losses on any investments that won’t recover | Potential to throw off your overall asset allocation |

Whether or not tax loss harvesting makes sense can be a complex calculation. If you’re thinking of giving it a try, consider speaking to a professional who can help you make sense of the ins and outs.

Suppose a stock you own takes a plunge, but you still want to own it. It might sound tempting to sell it—realize the loss for tax purposes—but then immediately buy it back again so you don’t miss out on gains.

To make sure investors aren’t gaming the system, the IRS has a rule about this. Per the so-called “wash-sale rule,” the IRS won’t let you claim a loss on your taxes if you reinvest the money back into the same investment (or one that is “substantially identical”) for 30 days before or after the sale.

So if you still want to own the investment you’re selling (or something similar), you can either wait until the 31st day or choose an investment that’s not identical to what you just sold.

Here’s what else you need to know about tax loss harvesting:

- Different tax rates apply to your profits, depending on how long you’ve held your investments.

- You generally have to use long-term losses to offset long-term gains (and short-term losses to offset short-term gains) before you’re allowed to mix and match.

- If your total losses are greater than your total gains for the year, you may be allowed to offset as much as $3,000 of your ordinary income (depending on your circumstances).

- If you don’t have enough gains to use up all your losses in a given year, you may also be able to “carry them forward” to reduce your taxes in future years.

Tax loss harvesting is a legal way to reduce your tax bill by strategically selling investments at a loss. That’s because the IRS lets you use your losses on some investments to offset your gains on others. Tax loss harvesting can be a complex strategy, and there are many ways for it to go haywire. Consider consulting the help of a professional if you’re considering it for your own portfolio.

- Stocks often perform better in January than they do in other months of the year. The so-called “January effect” may be due to tax-loss harvesting—investors sell losers in December in order to book a loss on the year’s taxes, then buy back those same stocks once they hit the 31-day mark in January.

- Around one million taxpayers will face an audit each year, so make sure your tax reduction strategies are on the up and up.

- You might have loved Beanie Babies, but creator H. Ty Warner didn’t love paying taxes. He pled guilty to tax evasion after failing to report $24.4 million in interest income.

- Tax loss harvesting is a legal strategy for reducing the taxes you owe on investments.

- With tax loss harvesting, an investor sells one investment at a loss and uses that to offset any capital gains they’ve realized on other investments.

- You can only use tax loss harvesting with realized losses—meaning losses you’ve locked in by selling an investment—not with investments that have fallen in price but that you still own.

- The IRS wash rule prohibits you from claiming a loss if you buy back the same (or a very similar) investment right after you’ve sold it (or within 30 days of selling it).

- Tax loss harvesting can help reduce your taxable income, but it’s complicated and might result in you missing out on future gains.