How to Start a Start-up

Go Big or Go Home

Although plenty of start-ups fail, the ones that succeed can do so wildly. Beyond a financial payoff, creating a start-up can give you the chance to create something meaningful, to disrupt the status quo—and, yes, even to change the world.

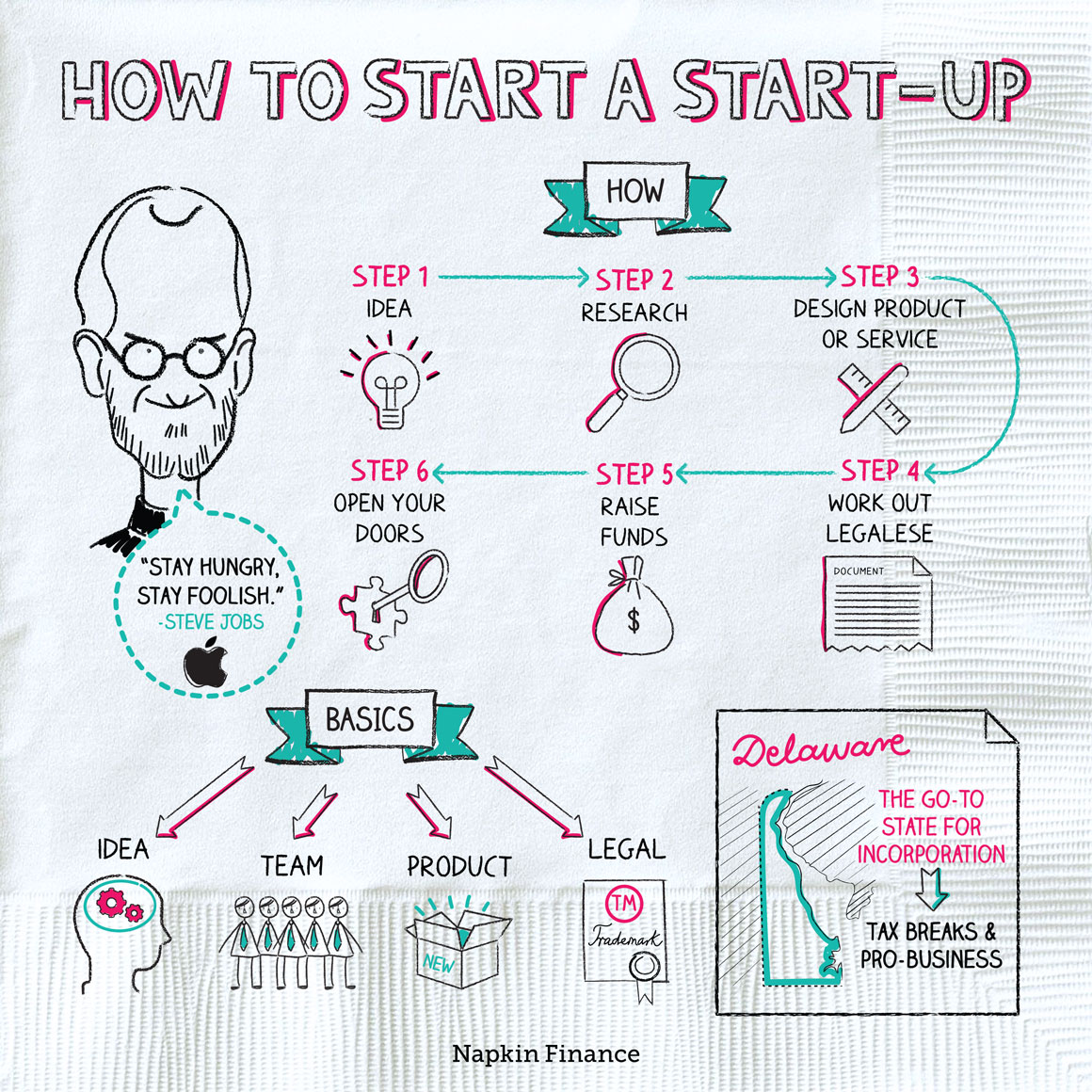

All start-ups are different, but most need each of these four things:

- Idea—maybe your start-up will disrupt an industry, make a product or service better, or meet a need that people didn’t even know they had.

- Team—find a group of people you can work with whose skill sets complement yours. Start with three main roles: business, technical, and creative.

- Product—develop a prototype of your product, a model for your service, or at least a realistic plan for how you’ll develop your first products.

- Legal—figure out your business structure, your name, and whether you need protection for your intellectual property.

“Because the people who are crazy enough to think they can change the world are the ones who do.“

—Steve Jobs

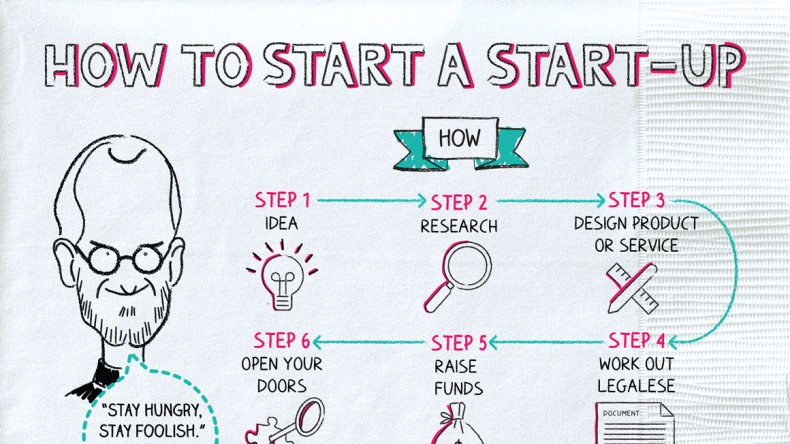

Here are the main milestones you’ll need to hit as you bring your new company to life:

Step 1: Come up with your idea.

Step 2: Research the market. Who would your competitors be? Who would your customers be? How strong might demand for your product or service be?

Step 3: Make a plan. Design your product or service.

Step 4: Figure out the legalese. Decide on a business structure. Pick a name and file for any licenses or permits.

Step 5: Raise funds. Do you want to sell ownership stakes or take on a loan?

Step 6: Get the word out. Create some excitement for your new business.

Step 7: Open your doors.

Although you may need a fresh idea, there are only a certain number of business models under the sun. Consider whether your company should:

- Sell ads—start a free website or app that draws people in and pay for it with ads.

- Create a marketplace—think Etsy or eBay.

- Sell goods or services to consumers—you could invent the next fidget spinner.

- Sell goods or services to businesses—solve a need for a specific industry.

- Go peer to peer—think Airbnb or ride shares.

- Sell intellectual property—develop something that you can license for a fee.

Your big idea probably needs some protection to make sure copycats don’t steal and profit from it. Depending on the products or services you offer, here’s what you might opt for:

| Type | What it covers | How it protects you |

| Trademark | Words, phrases, symbols, and devices | A trademark can stop other companies from making similar products under the same name. (Hint: You can’t call your revolutionary sneaker a Nike.) |

| Copyright | Original artistic works, such as songs, paintings, and software code | You get exclusive rights to reproduce or profit from the protected work. While your original work gets an automatic copyright at the time of creation, formal registration gives you better protection. |

| Patent | Discoveries and inventions (but not ideas) | Gives you a temporary monopoly over the invention (and any profit from it). A patent goes to the first person to file, so don’t drag your feet. |

Starting a start-up is exhilarating and exhausting. You probably don’t want to think about the F-word: Failure. But keeping that at bay depends on taking a look at your startup after launch (and periodically thereafter) to figure out what changes to make to keep growing.

Look at your sales, customer feedback, and market dynamics. Ask yourself whether your product or service is succeeding the way you’d hoped or how you can improve it. You might learn that your “perfect” idea isn’t so perfect after all. But pivoting your product or making other needed changes could be the difference between growing and petering out.

Launching a start-up gives you a chance to build your dream, disrupt an industry, or change the world. It all starts with your idea—followed by careful research and business planning, getting the legal pieces in order, finding funds, and opening your doors. There are various types of business models you can pick, and they can all benefit from a careful review to keep the company running smoothly.

- There are more “unicorn” companies—meaning startups worth $1 billion or more—based in California than anywhere else in the world.

- Many companies choose to incorporate in Delaware (even if they’re headquartered elsewhere) because the state has a well-developed corporate law system and charges no income tax on companies that don’t do business there.

- Launching a start-up can give you a chance at making it big.

- To start a new company, you first need an idea, a team, a product, and some help with legalese.

- Although it may seem difficult to come up with an idea, you can get inspiration from existing business models.

- Getting a patent, copyright, or trademark for your idea can offer extra protection against someone profiting from your creativity.

- Reassess your start-up periodically to make sure you’re meeting your goals and continuing to grow.