Financial Advisors

Get Some Help

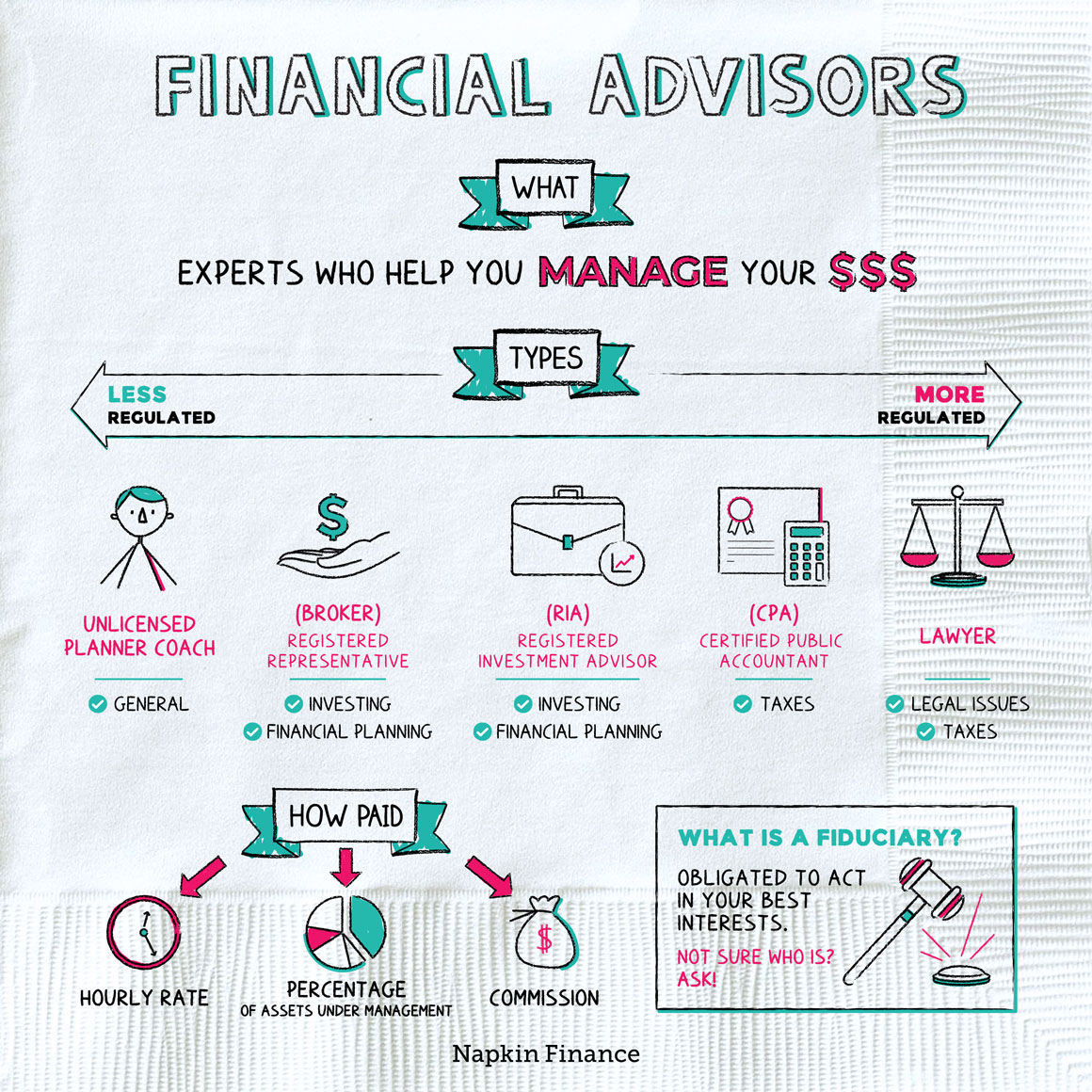

Financial advisors are experts who can provide financial advice and help you manage your money.

Some people have an ongoing relationship with a financial advisor, whom they meet with a few times every year. Others may prefer to handle most of their financial decisions themselves and only consult with an expert from time to time for specific problems.

Different financial advisors can help with:

- Choosing and managing investments

- Saving for a kid’s college education

- Figuring out how you’ll pay for retirement

- Taxes

- Creating a will, trust, or broader estate plan

- Choosing insurance

- All-around financial organization—from making sure that you’re staying on top of your different accounts to helping you figure out the best way to pay down debt

The phrase “financial advisor” can encompass a wide range of professionals—some of whom may have had to pass strict licensing exams and others who may have few or no credentials. (Some financial advisors aren’t even real live humans, although so-called robo-advisors typically don’t handle nuanced financial planning issues.)

The main types of financial advisors include:

| Who | Expertise | Legit? Well regulated? |

What they do |

| Certified Public Accountants (CPAs) |

|

|

|

| Lawyers |

|

|

|

| Registered Investment Advisors (RIAs) |

|

|

|

| Registered representatives (aka brokers) |

|

|

|

| Unlicensed planners or coaches |

|

|

|

In addition to holding some kind of specific license, many financial advisors possess additional credentials, such as:

- CFP certification—A Certified Financial Planner has completed classes and passed an exam on a broad range of financial planning issues.

- A CFP may be a good bet if you’re looking for holistic planning.

- CFA charter—A Chartered Financial Analyst charterholder has passed several rigorous exams on investing and must abide by a strict code of ethics.

- A CFA charterholder could be the right choice if you’re looking for deep-dive investing help.

Fees for financial advice can vary widely—both in terms of how much advisors charge and how their fees are structured.

The most common fee structures are:

- Percentage of assets under management

- An RIA or broker could charge a 1% annual fee. If you had $100,000 invested with that advisor, he or she would earn $1,000 per year.

- Hourly rate

- This is typical for CPAs and lawyers. Some financial planners also work this way.

- Commission

- Some brokers and RIAs earn a commission when they sell you a new investment.

- Many experts argue that this type of fee structure creates the worst types of conflicts of interest and can hurt clients.

Here are some steps you can consider taking if you think you’d like to work with an advisor:

Step 1 → Figure out what you need. Decide if you’re looking for broad financial planning or help with a specific problem.

Step 2 → Cast your net. Ask people in your area for referrals. Check national or statewide professional networks—such as your state association of CPAs—for names.

Step 3 → Do some initial due diligence. Once you’ve got a few candidates, check their credentials. Make sure they actually hold the licenses or certifications they claim to, and check with regulators or professional organizations to see if they’re in good standing or have any complaints listed against them.

Step 4 → Meet your remaining candidates. Make sure they can provide the services you’re looking for, and make sure you’re crystal clear about how they get paid.

Step 5 → Ask for references to other clients. Then pick up the phone and actually call those references.

Step 6 → Enjoy your match made (hopefully) in heaven.

A fiduciary is someone who is legally obligated to act in your best interest, even if that means putting your financial interest ahead of his or her own.

Some financial advisors are fiduciaries, and others aren’t. Although choosing an advisor who’s a fiduciary may not guarantee that you receive the best advice, it can provide an extra safeguard.

How do you know who is a fiduciary and who isn’t? Just ask.

Financial advisors can help you with specific money questions or with simply untangling the mess of your finances. When choosing a financial advisor, it’s important to make sure you choose the right kind of expert (or generalist) who can provide the help you need and to make sure that you understand how your advisor gets paid.

- John Oliver thinks you should always make sure your advisor is a fiduciary, and make sure you don’t pay more than 1% in fees per year total.

- In 2019, the owners and directors of an alleged $1.2-billion real estate-based ponzi scheme called Woodbridge Group were arrested. The firm allegedly relied on a network of unregistered brokers—some of whom had previously been registered but had their licenses revoked due to misconduct—to sell fake investments to senior citizens. (Like we said—always make sure your advisor is actually licensed!)

- In addition to outright stealing client funds, some of the ways bad actors can rip off clients include placing client funds in whatever investments pay the highest commissions and excessively trading, or “churning,” to boost fees.

- Financial advisors can help with investments, insurance, taxes, and general financial planning issues.

- “Financial advisor” is a catchall term that can include investment advisors, brokers, tax experts, attorneys, and others.

- When choosing an advisor, it’s important to make sure you understand your advisor’s particular areas of expertise and how your advisor gets paid.

- Many people choose to work with advisors who have a fiduciary duty to clients, meaning they are obligated to place clients’ financial interests ahead of their own.