529 Plan

Higher Ed, Higher Returns

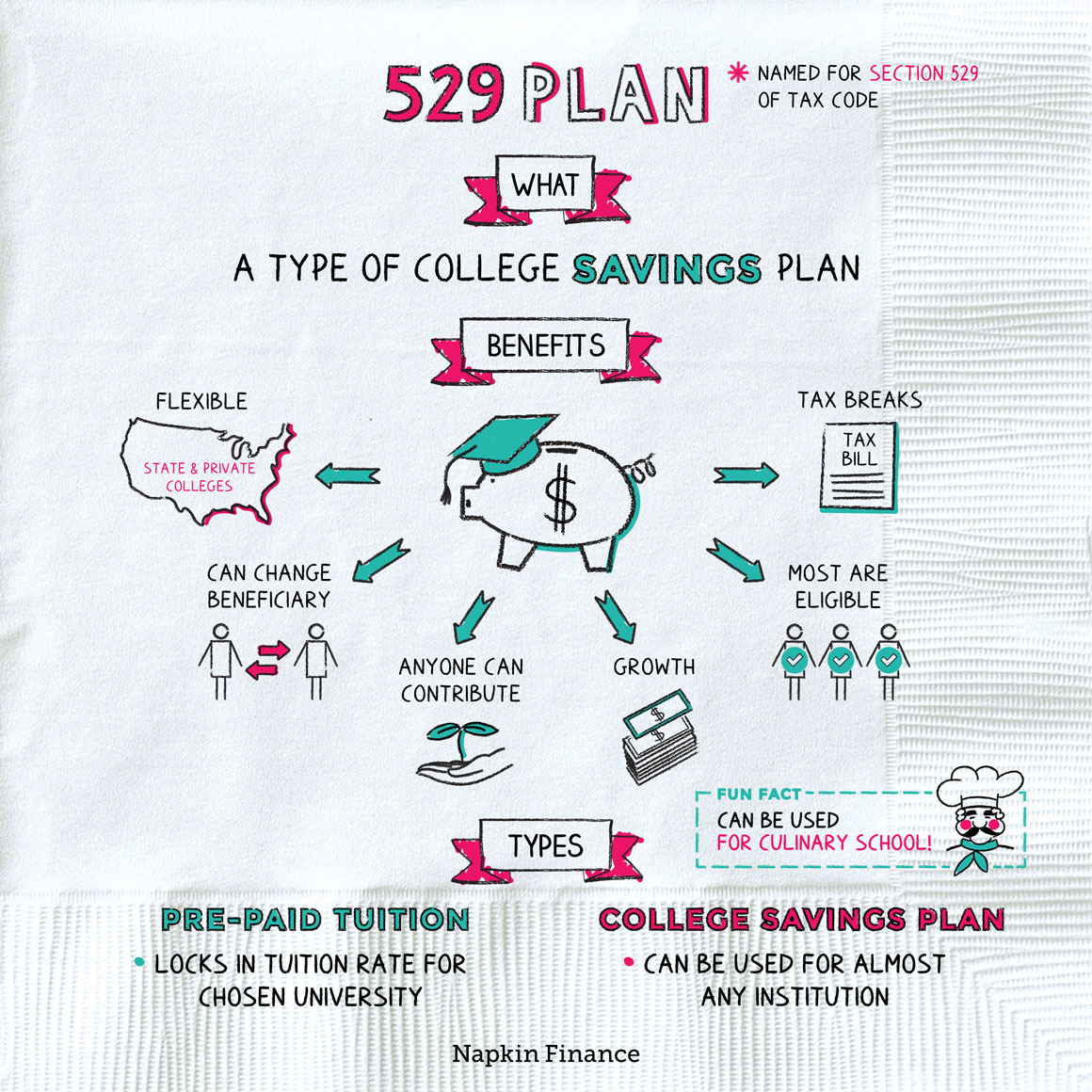

A 529 plan is a tax-advantaged college savings account sponsored by a state government or education institution. The plans are kind of like 401(k)s for college funds. (The name comes from the section of the tax code that authorizes the accounts.)

There are two types of 529 plans:

- Savings plans, which let you build up assets that you can use toward almost any U.S. college

- Prepaid tuition plans, which can let parents pay today’s tuition rates for a child’s future education (but may limit where a child can go to school)

Not surprisingly, the more flexible savings plans tend to be more popular.

529s can offer several significant advantages, including:

- Tax breaks—Your money can grow tax free in a 529 account and be withdrawn tax free as long as you use funds for qualifying expenses. Depending on which state’s plan you choose and what state you live in, you may also get a state tax deduction on contributions.

- Potential growth—You typically have a number of investment options to choose from in a 529 plan, so your money can grow.

- No restrictions on who can contribute—Grandma’s birthday check can go straight into the 529.

- Few restrictions on eligibility—Even high-income families can use the plans.

- Flexibility—You can invest in any state’s 529 program. And funds from any state’s plan can be used at any of more than 6,000 schools.

- Ability to change beneficiary—If a child (or other beneficiary) doesn’t end up going to college, you can change the beneficiary to anyone else (including yourself).

The only significant drawback is that the plans place restrictions on withdrawals. If you withdraw money for noneducational expenses, you’ll typically pay a 10% penalty plus income taxes on any withdrawn earnings.

Anyone—a parent, grandparent, sibling, distant relative, kind neighbor—can open a 529 account. You can even open one for yourself. Here’s how:

Learn about your state’s 529 plan

↓

Compare your state’s plan to other states’ plans available to nonresidents

↓

Choose a plan and open an account (online or by mail)

↓

Pick your investments

↓

Make your first deposit

The last two steps might flip-flop depending on the plan you pick. Some want to first know where to put your money once they get it, and other plans want to get your initial deposit before letting you choose investments.

Once you have an account, you can set up automatic recurring deposits or make additional contributions manually whenever you happen to have funds available. You can also change how the money you hold in the plan is invested but only twice per year.

With all the 529 plan options out there, it might seem tough to pick the right one. Experts recommend that you start by looking at your state’s plan because there could be more tax benefits for you.

If you want to compare different plans within your state (if there are multiple plans) or between states, here are some questions to help you pick the best one:

- What are the plan’s tax perks?

- What fees does the plan charge and when?

- What investment options are available?

- Does the plan offer matching grants or other benefits?

- Are there minimum or maximum contribution limits?

If you’re really struggling to decide, there’s nothing stopping you from opening multiple 529 accounts in different states. Just don’t contribute more than someone could reasonably use for education expenses (unless you want a friendly visit from the IRS).

529 plans can be a great way to save for college. There are many out there to consider, and most come with tax benefits and other advantages.

- 529 assets can be used to pay for vocational school—including some culinary, acting, and massage therapy schools (but not any clown colleges).

- You can also use the assets at a handful of schools abroad, including for a destination education at some schools in the Cayman Islands, St. Maarten, and St. John.

- Parents tend to save more money toward boys’ college educations than toward girls’ college funds.

- 529 plans can help families save for college.

- The more popular type, 529 savings accounts, is like a 401(k) for college.

- The other type, 529 prepaid tuition plans, lets parents pay tuition now for their kids’ future education.

- Each 529 plan has its own tax benefits and incentives but also its own contribution rules and investment options.