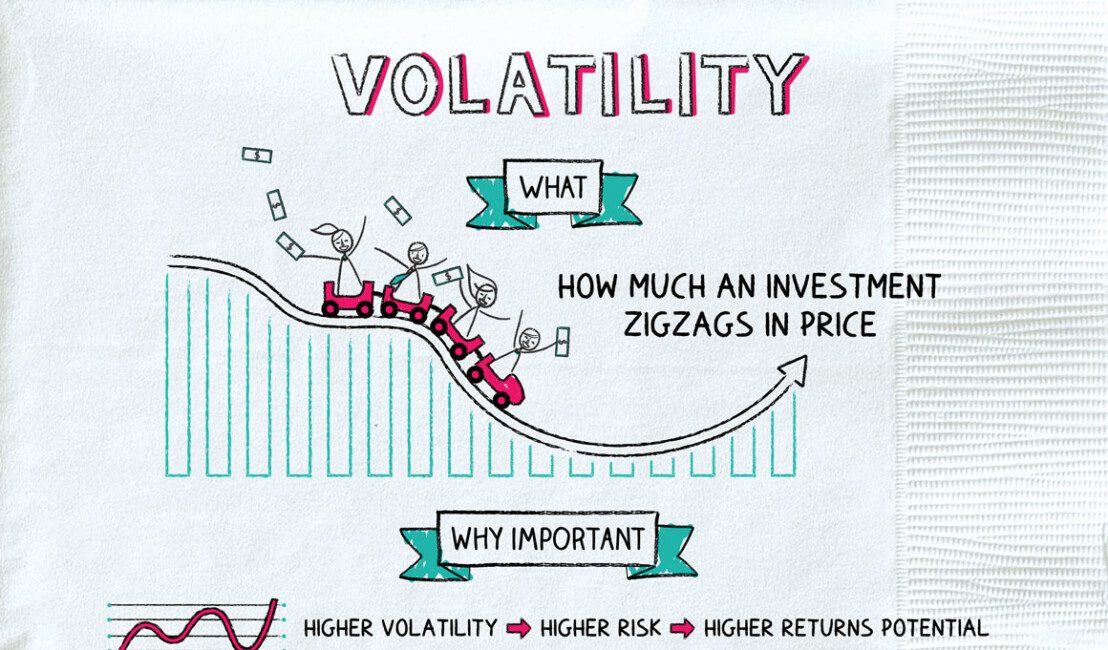

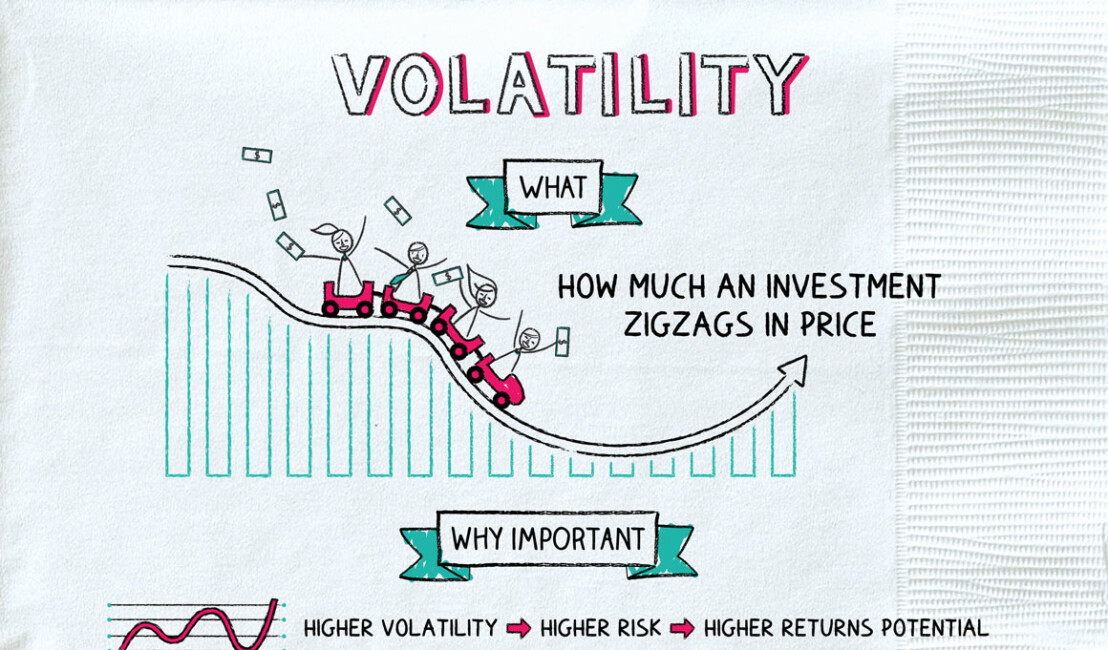

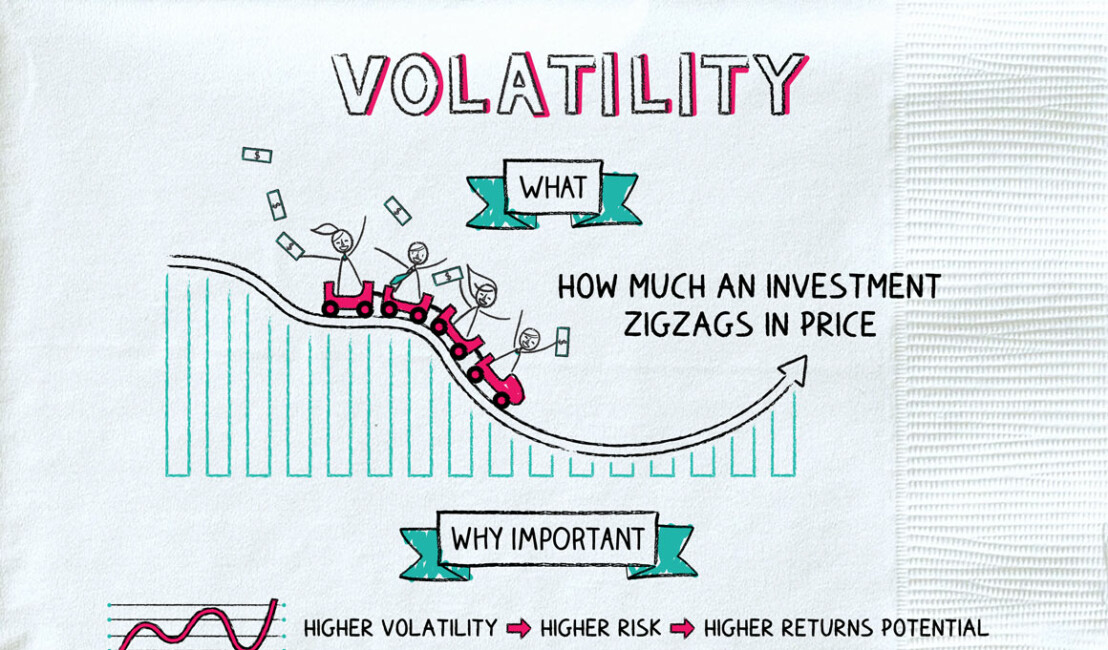

Volatility: Buckle Up

August 27, 2019

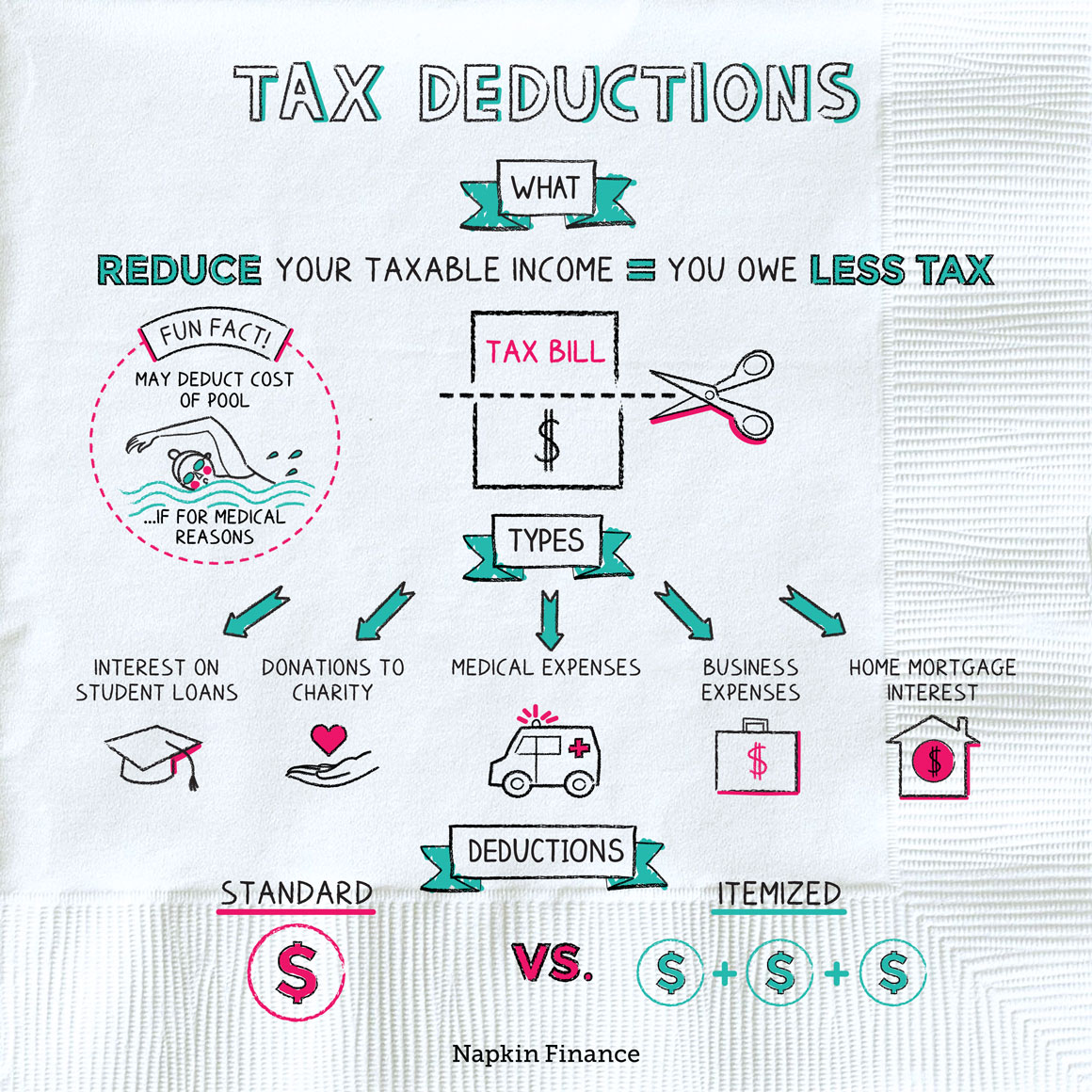

One of the biggest decisions you’ll make when you file your 2019 taxes is whether to take the standard deduction or itemize your expenses.

The standard deduction is a flat number set by the IRS based on your income. If you don’t have a lot of deductible expenses, taking the standard deduction is the straightforward route.

That might seem like the way to go — after all, no one wants to spend more time on their taxes than they have to. But itemizing makes more sense if your allowed expenses add up to more than the standard deduction. Potential deductions include health insurance premiums, student loan interest, state and local taxes, mortgage interest, and charitable donations.

You can get away with some pretty funky deduction claims. Things that don’t qualify, though? Weddings, dogs, and fallout shelters. And yes, people really did try to get these by the IRS.

https://www.davisvanguard.org/

https://www.kimiafarmabanten.com/

https://www.kimiafarmabanten.com/

https://www.kimiafarmabatam.com/

https://www.kimiafarmabogor.com/

https://www.kimiafarmajambi.com/

https://www.kimiafarmalampung.com/

https://www.kimiafarmamedan.com/

https://www.kimiafarmapalembang.com/

https://www.kimiafarmapontianak.com/

https://www.kimiafarmariau.com/

https://www.kimiafarmasurabaya.com/

The simple information you need

to clean up your not-so-simple finances.