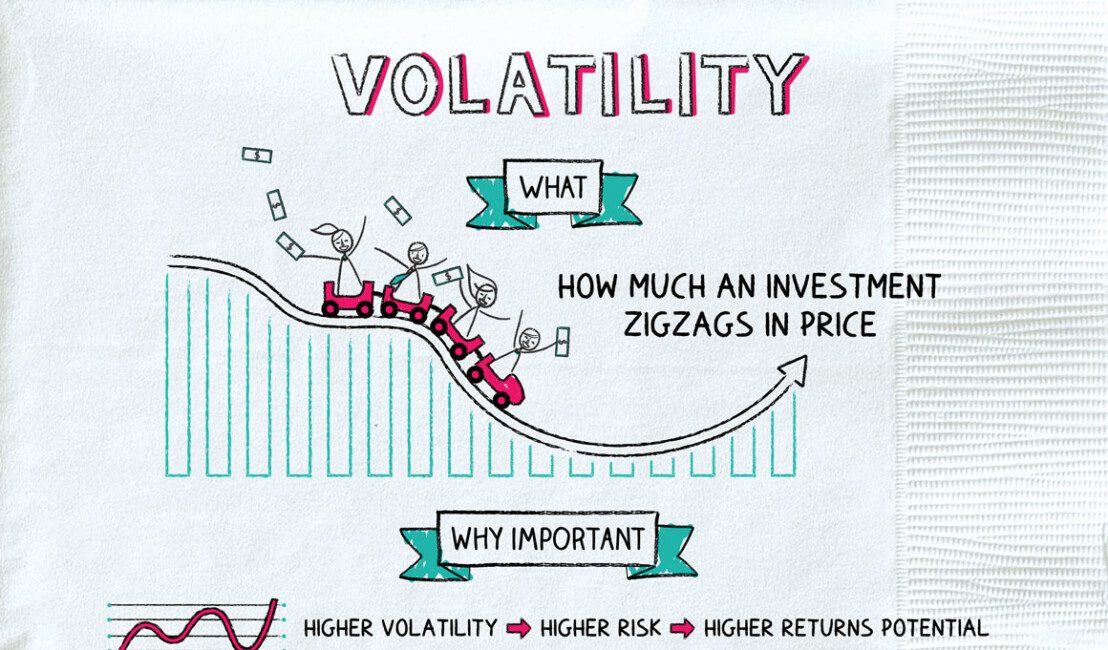

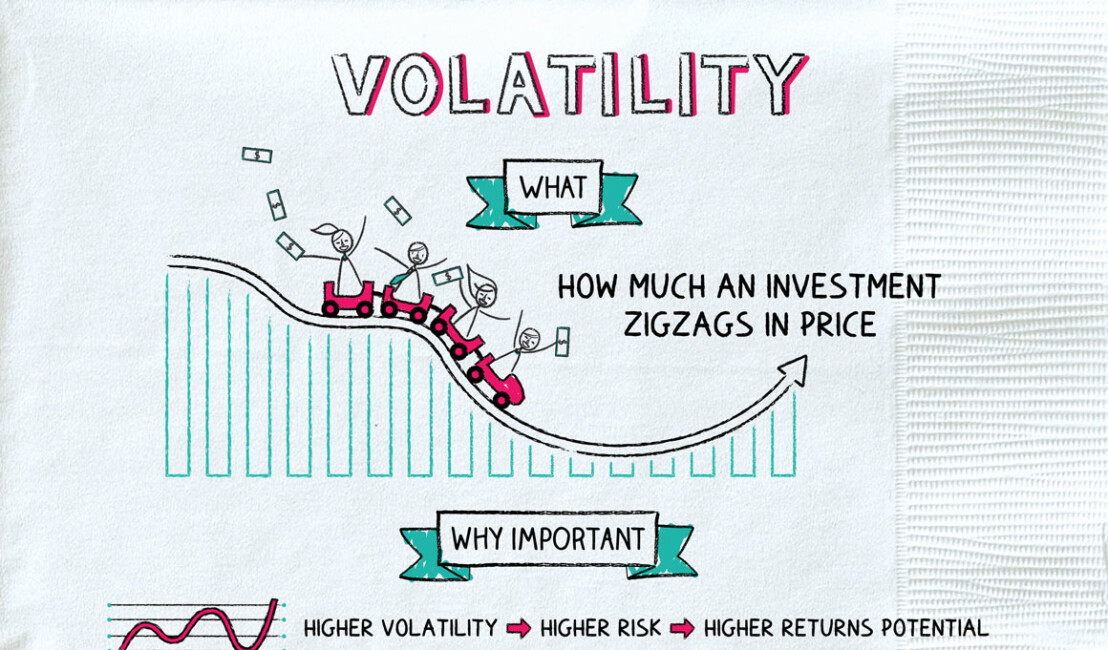

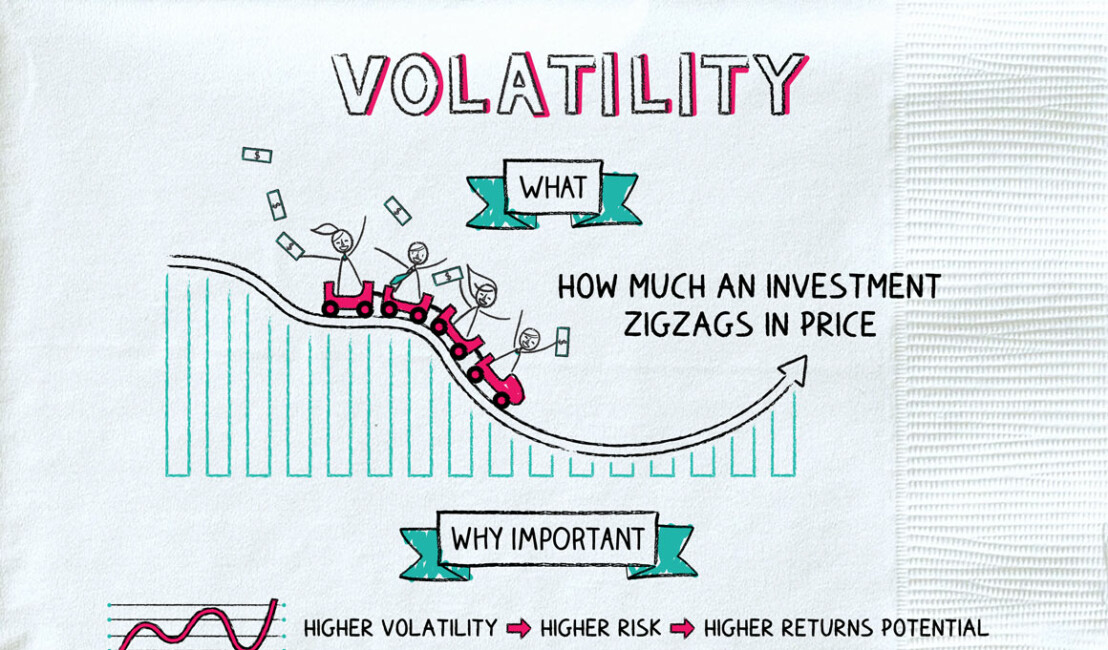

Volatility: Buckle Up

August 27, 2019

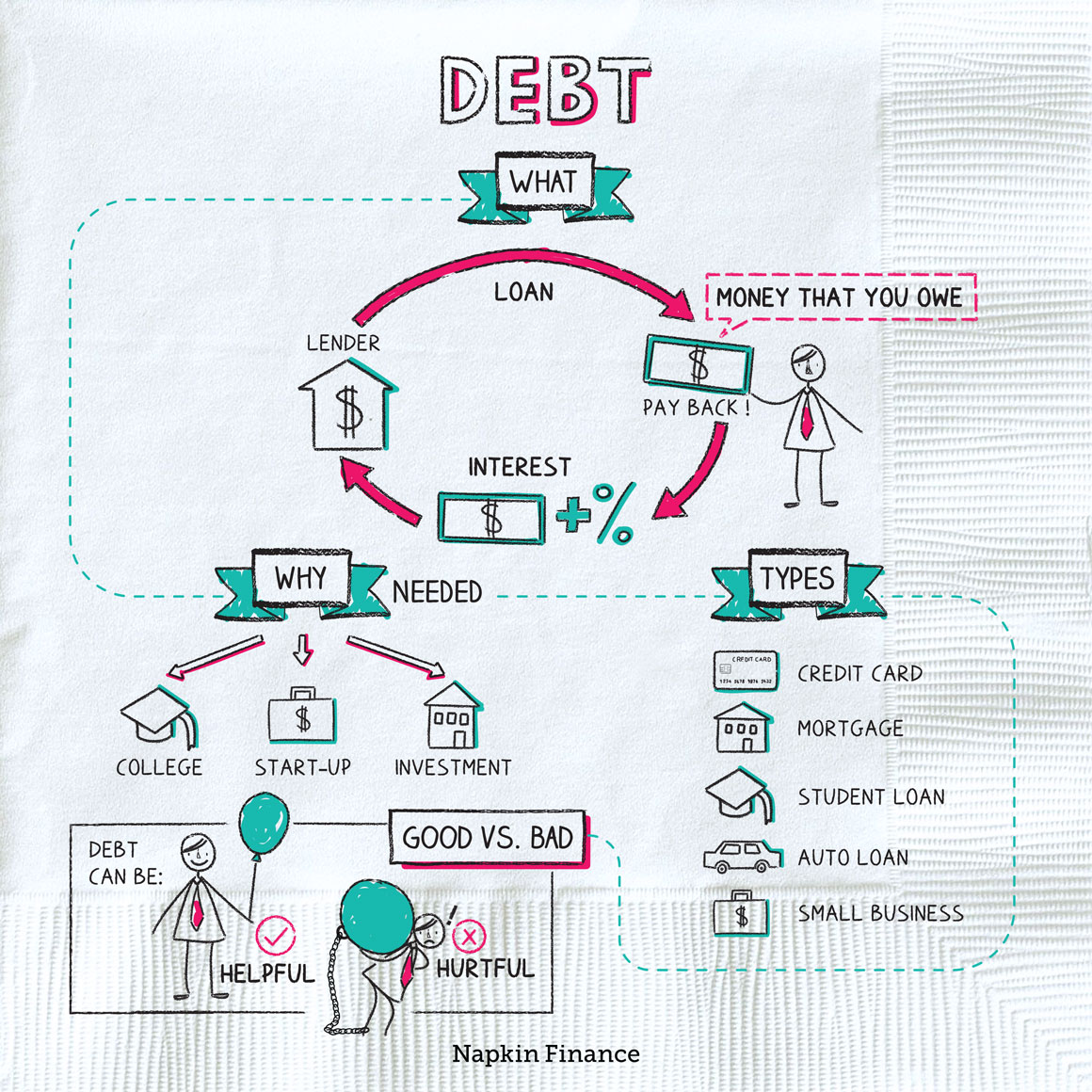

For the 15% of consumers who are only making the minimum payment, that balance could take as much as a decade to pay off. But it’s still a drop in the bucket compared to the almost $900 billion total tab Americans carry on credit cards and other forms of revolving debt.

https://www.davisvanguard.org/

https://www.kimiafarmabanten.com/

https://www.kimiafarmabanten.com/

https://www.kimiafarmabatam.com/

https://www.kimiafarmabogor.com/

https://www.kimiafarmajambi.com/

https://www.kimiafarmalampung.com/

https://www.kimiafarmamedan.com/

https://www.kimiafarmapalembang.com/

https://www.kimiafarmapontianak.com/

https://www.kimiafarmariau.com/

https://www.kimiafarmasurabaya.com/

The simple information you need

to clean up your not-so-simple finances.