What is a credit rating?

It measures the ability of a borrower to repay money. A high rating means that there is a lower risk of the borrower defaulting (being unable to make the required payments) on his or her debt and is therefore good while a low rating means the opposite – there is a higher risk of defaulting.

How is the rating expressed?

For individuals, the rating is usually expressed as a range of numbers – this is called a score. A score is derived from a person’s history maintained by reporting agencies such as Equifax, Experian, and TransUnion.

For businesses and the government, ratings are expressed as letters. Since different agencies can assign ratings, there is not a set range. For example, Standard & Poor’s (S&P) rating ranges from AAA (great) to C (poor). On the other hand, Moody’s rating ranges from Aaa to D.

Why is your rating important?

Your rating can affect everything from approval for a loan to the amount of interest charged. It’s important to make sure that your rating is the best that it can be.

Calculator: Who wants to be a millionaire?

[wpdatatable id=18]

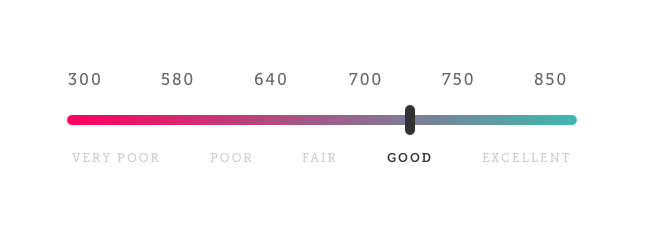

Score scale

Tips for building a good credit rating

- Open a bank account. Lenders may want to see evidence of consistent savings.

- Only apply for new credit cards when you need them. Credit scores go down every time you open a new credit card.

- Pay all your bills on time.

- Keep the balances on your credit cards low.

- Apply for small or incremental loans and repay them on time.

- Consider asking for a cosigner with an established credit history to get lower rates on large loans.

- Secure a steady job. Lenders may ask for employment information.

- Be vigilant about payments. Careless mistakes can affect your score for a long time.

[toggles heading=’References’]

- http://money.usnews.com/money/blogs/my-money/2010/07/15/9-surprising-facts-about-your-credit-score

- http://www.investinganswers.com/financial-dictionary/debt-bankruptcy/credit-rating-1213

- http://www.credit.com/credit-scores/what-is-a-good-credit-score

[/toggles]