Lesson 5: Types of investment accounts

Before you can invest, you have to open an account.

The biggest difference between types of investment accounts is how they are treated for tax purposes and when you can withdraw your money. Here are the three main types of accounts:

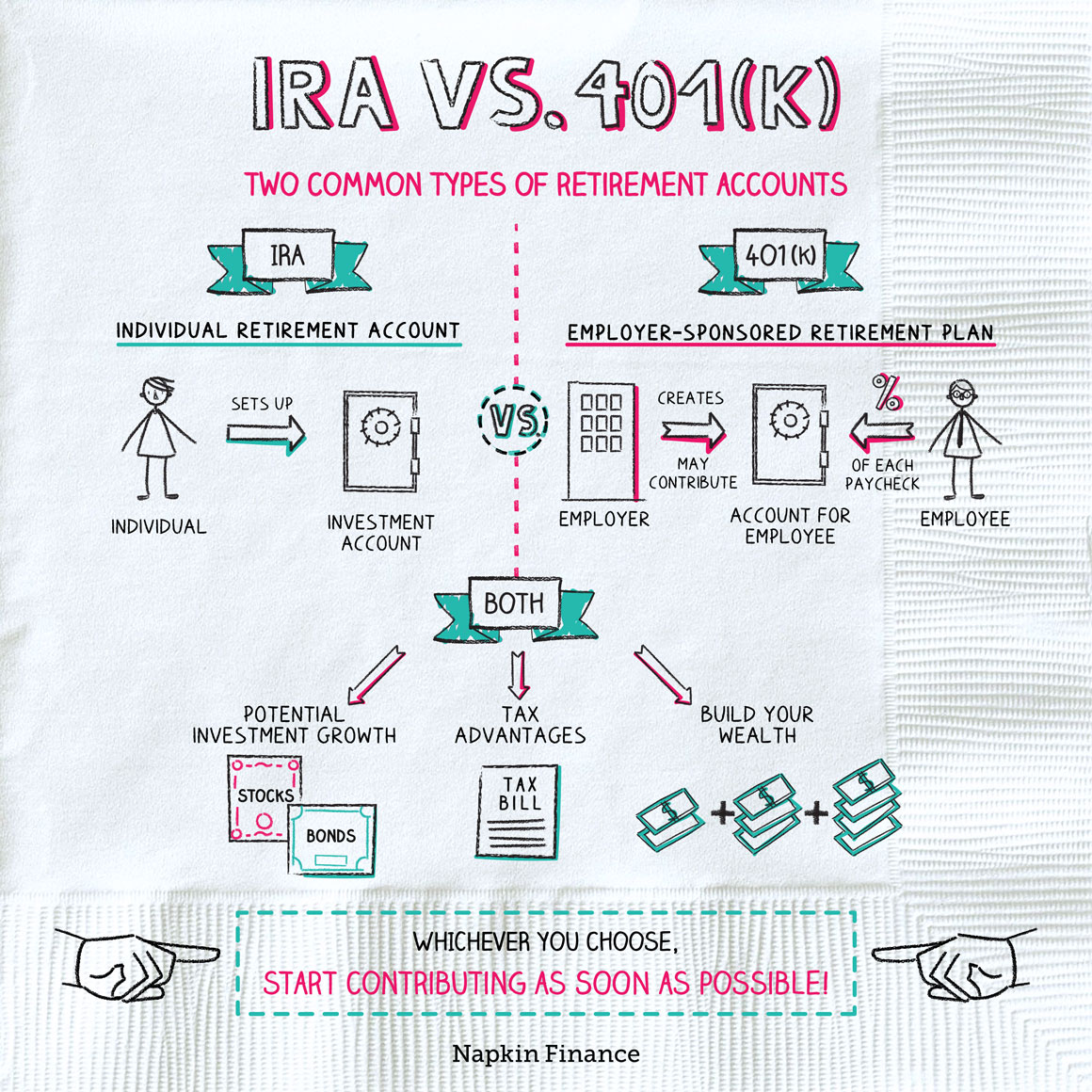

401(k)

To invest in a 401(k), you have to be eligible for one through your employer. With a 401(k), contributions are taken out of your paycheck before taxes. The other basic features of a 401(k) include:

- No taxes on investment gains or income

- Withdrawals are taxed

- Max. annual contribution of $18,500 up to age 50 ($24,500 if you’re 50 or older)

- Penalties on any withdrawals taken before age 59½

- Investment choices may be limited

Besides tax breaks, the big advantage of a 401(k) is the potential for free money: Many employers match your contribution dollar for dollar up to a certain amount.

Let’s say your company offers a 4% match. Here’s what that looks like in practice, with sample dollar amounts if you earned around $50,000 per year.

| If you contribute . . . | Your employer will contribute . . . |

| 0% of your paycheck ($0) | $0 |

| 2% of your paycheck ($42) | $42 |

| 4% of your paycheck ($83) | $83 |

| 10% of your paycheck ($208) | $83 |

If your employer offers a match, it’s crucial for you to contribute enough to at least capture the full match. Not doing so means missing out on thousands of dollars of free money (which, thanks to compounding, will grow into tens of thousands by the time you retire).

IRA

The other main way to save for retirement is through an individual retirement account (IRA). As the name suggests, IRAs aren’t linked to your employer, so you’ll need to set yours up on your own.

And the first question you’ll face is whether you want a Roth or a traditional IRA. Here are the major differences between the two:

| Roth IRA | Traditional IRA |

|

|

Trying to decide which one is right for you? Some experts recommend contributing to a Roth IRA when you’re in your early earning years (because they assume you’ll earn more and be in a higher tax bracket in retirement).

Taxable brokerage account

An ordinary brokerage account is easy to open but doesn’t come with the tax perks of a retirement account. The pros and cons include:

Pros

- No complicated eligibility or withdrawal rules to keep track of

- Easy to fund

- Can withdraw money at any time

- Unlimited investment choices

Cons

- Owe taxes anytime you sell an investment for a profit or receive income from your investments

- No employer match

Because the tax advantage of retirement accounts is so great, experts generally recommend that you fully fund your retirement accounts before opening a traditional brokerage account.